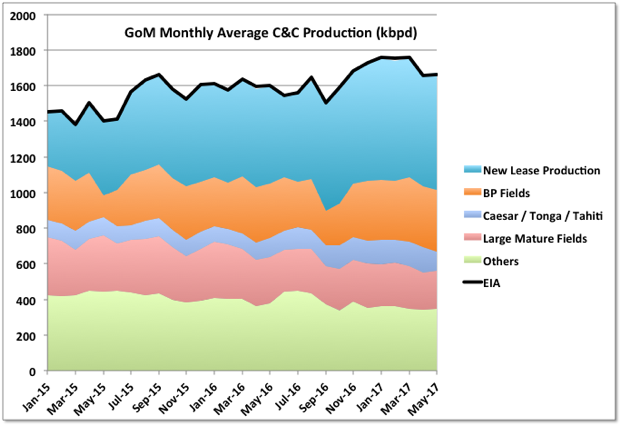

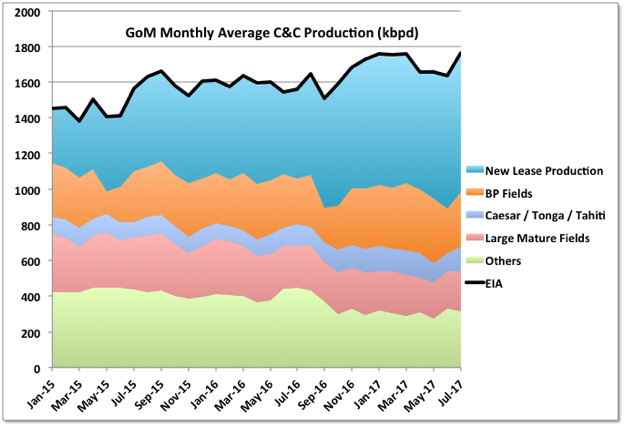

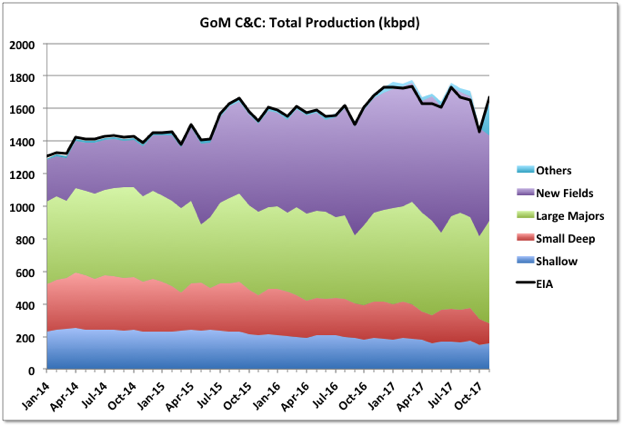

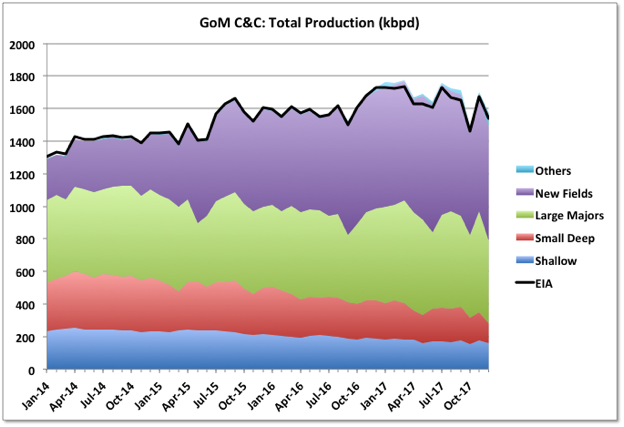

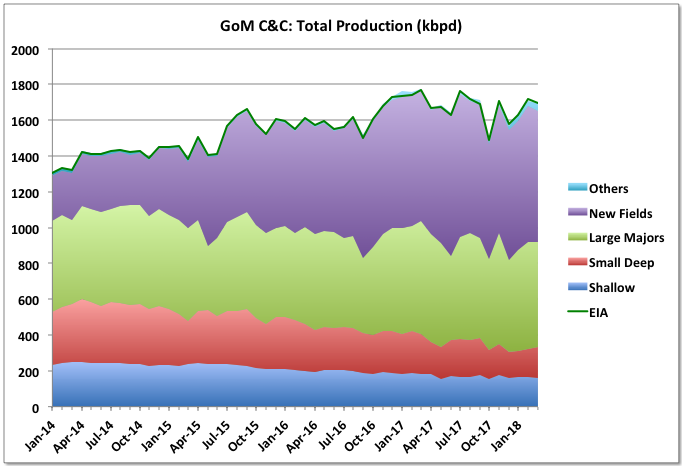

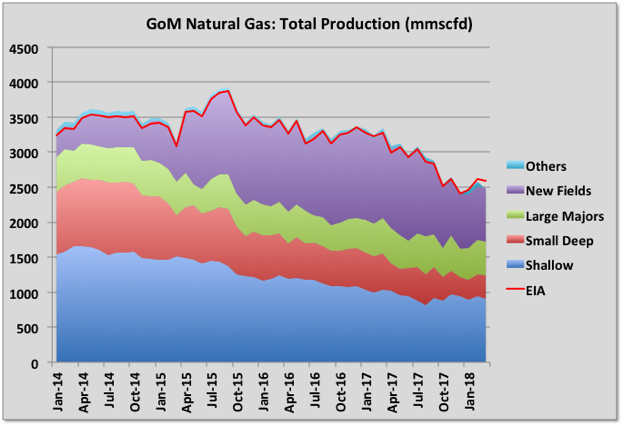

Production for May by BOEM was 1673 kbpd and by EIA 1661, compared with 1661 and 1658 kbpd, respectively in April.

March looks like the peak, at least near term, for the basin, especially with Hurricane Cindy impacting the coming June figures.

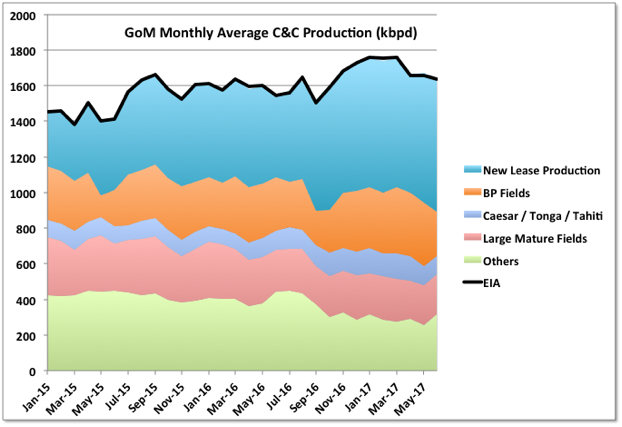

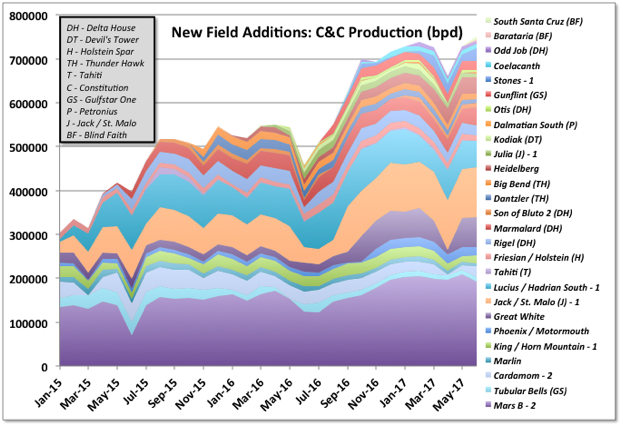

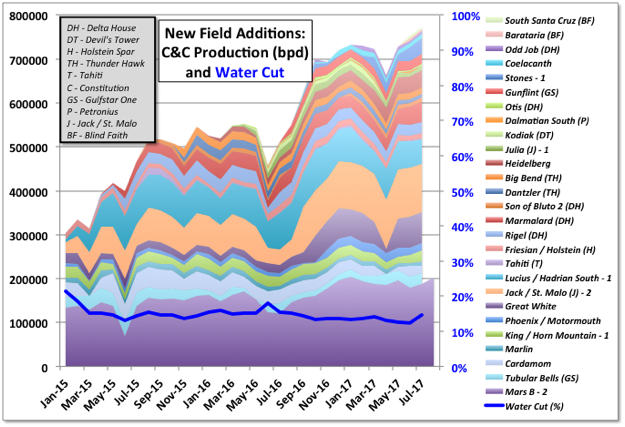

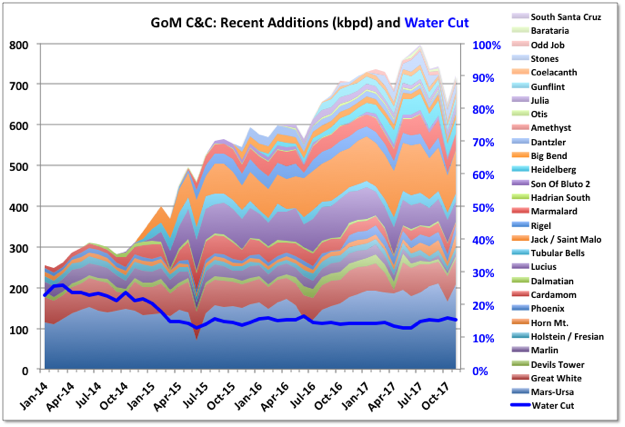

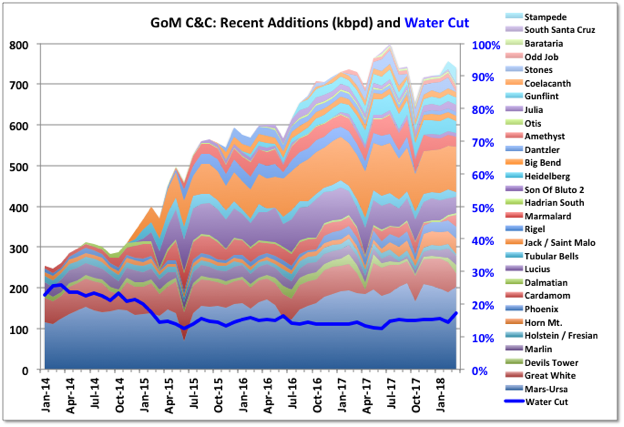

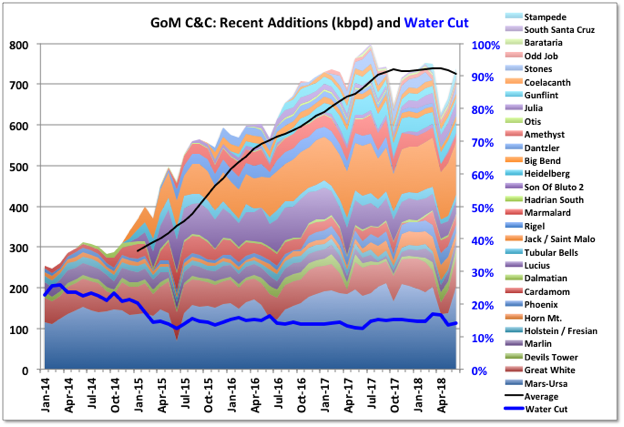

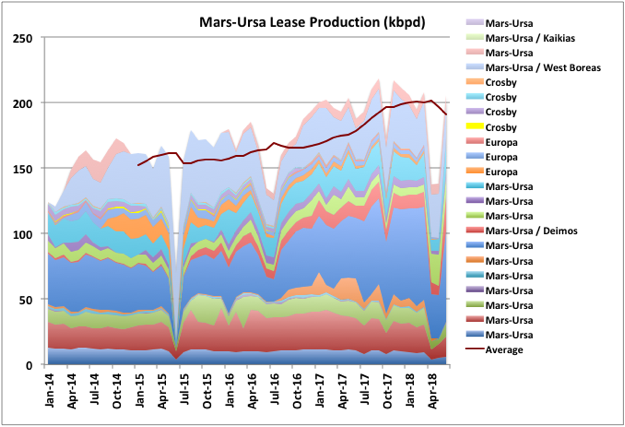

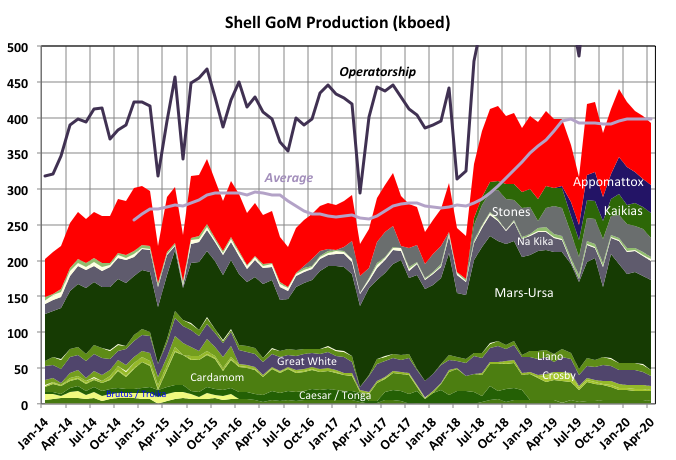

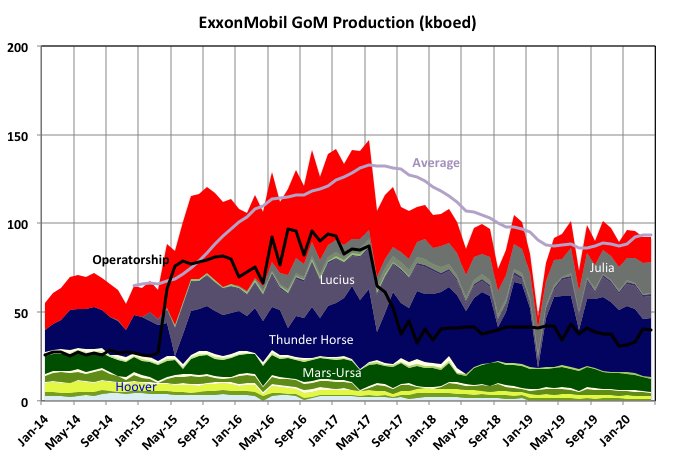

The combined new fields added from late 2014 look to be peaking as well. Great White came back on line but xxx and yyy declined. In previous data I had omitted one big producing lease in Mars, which included the new Deimos field. With this added the production growth through 2017 is higher (and as shown later the decline in mature fields faster) than previously shown. There may be more increase to come: the Mars leases had three rigs operating through June, one dedicated for Deimos, which has now gone. The two platforms on the field each have a dedicated platform rig, so they can continue with in-fill drilling and workovers as they wish. The Kaikias development will be tied into the Olympus TLP on the Mars field in 2019, but it’s a subsea tie-back so would need a separate drilling rig. The facility has nominal capacity of 100 kbpd, but that might be limited by the platform wells and manifolds rather than production trains – if not then Shell must be expecting some decline before Kaikias comes on line.

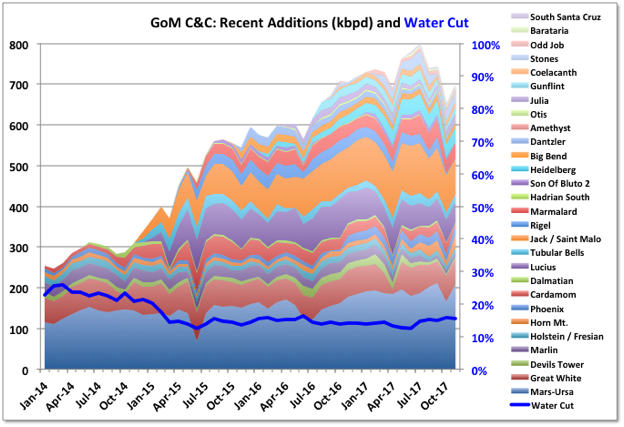

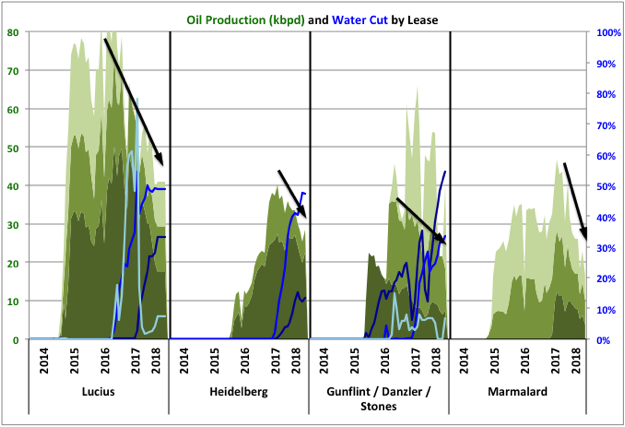

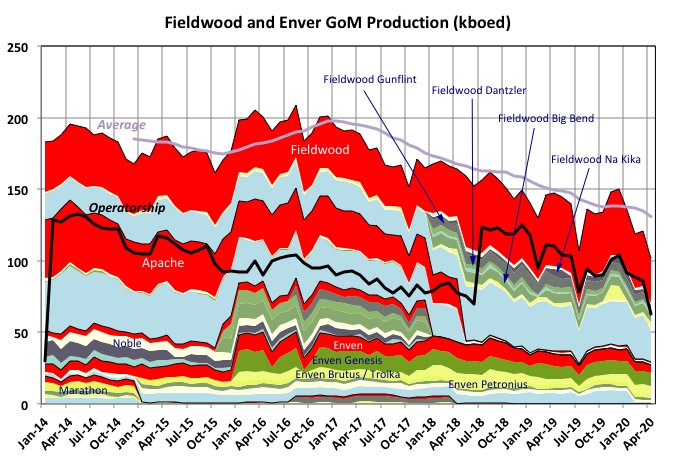

Stones start-up is still not looking good with an 8 kbpd fall – Shell are taking over the operation from SBM by buying the FPSO instead of leasing. Maybe this indicates poor operating performance (if so it’s something for ExxonMobil to be concerned with as they are following the same approach with SBM for Liza), or maybe just a convenient scapegoat. Julia, Cardamom, Stones, Jack and Lucius still have active drilling programs so may have opportunity for growth. Julia had plans for subsea multiphase pumping, I don’t know if that is operating or will be brought on as pressures fall.

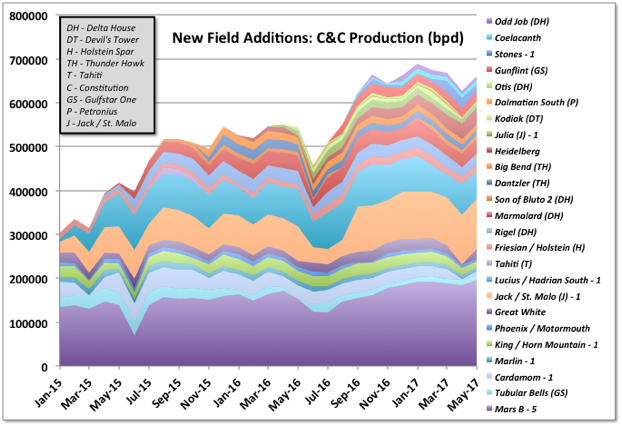

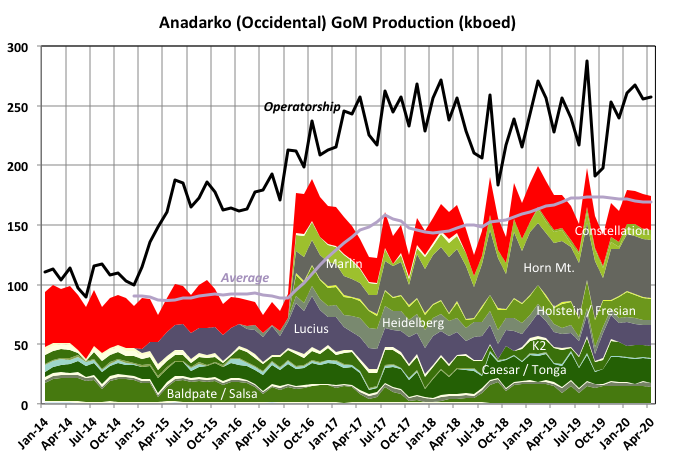

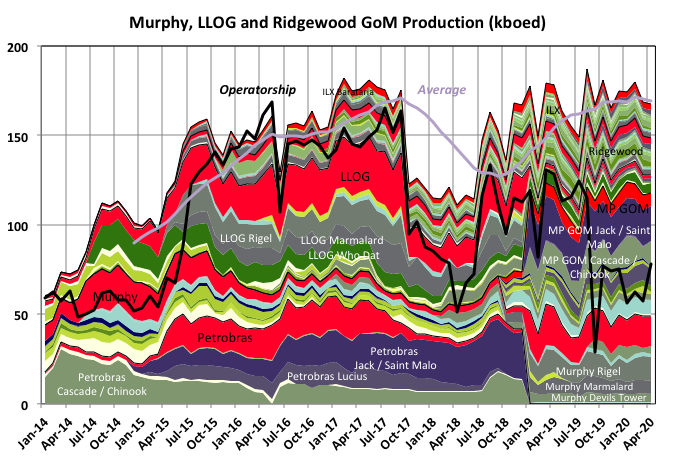

Production from the South Santa Cruz and Barataria fields started in mid June (actually part of Fourier and East Anstey fields by BOEM naming). The first Horn Mountain Deep well, for Anadarko, started production in April, a second well is due to be spudded this quarter. These are the only new fields announced for this year. Anadarko was the only company that had hinted they may develop something else (e.g. with Warrior and Phobos tie backs), but with them slashing budgets for 2017 after poor second quarter results that is now be unlikely: in their investor presentation they indicated they expected flat production out 3 to 5 years, and didn’t sound particularly confident of that to me, and with no mention of Shenandoah so that might be on the way to full cancellation. One new lease in the Marmalard field (the last there) for LLOG was started in late May.

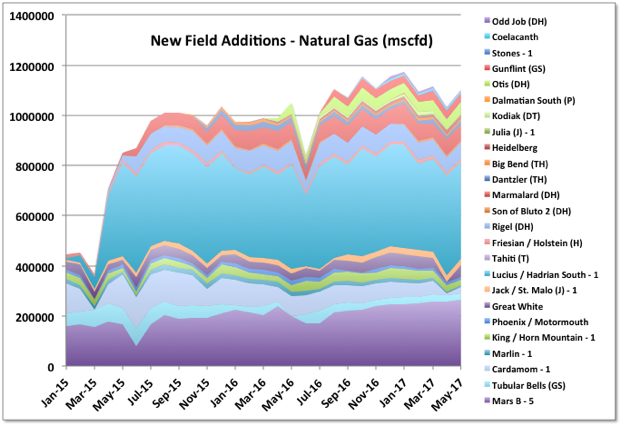

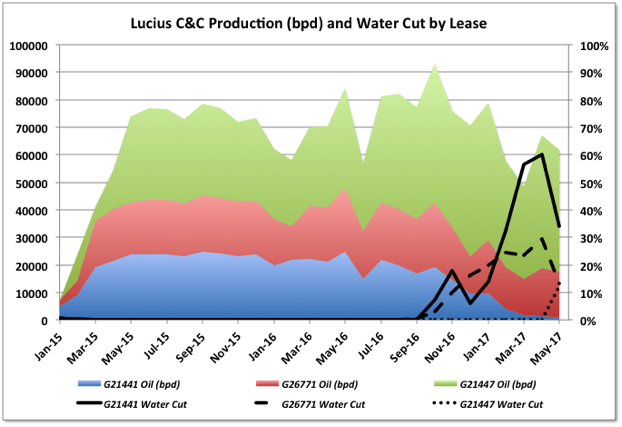

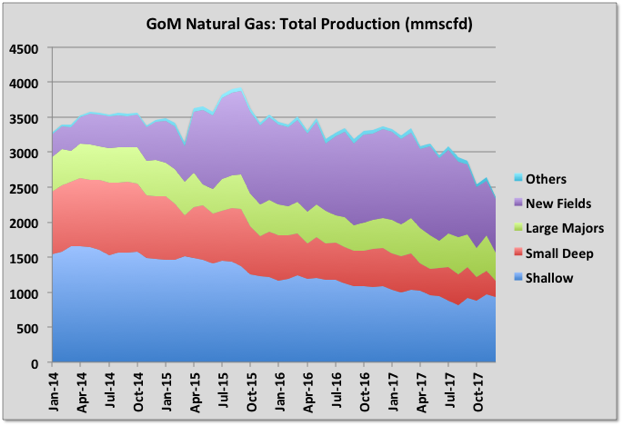

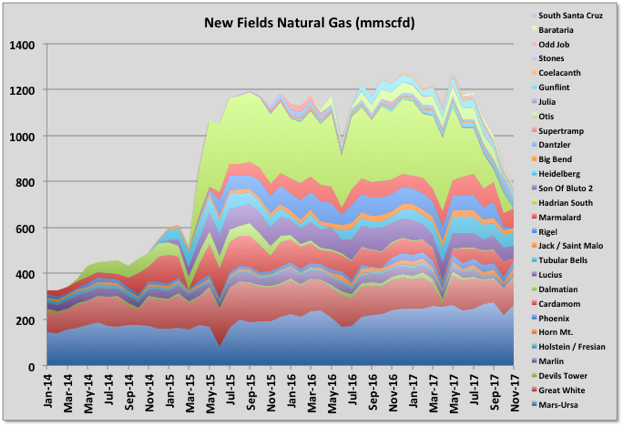

I’ve added natural gas production for the new fields here. Hadrian South and Otis are the only dedicated gas fields. Hadrian South production is a big proportion of the gas total from GoM now. It produces to the Lucius Spar, operated by Anadarko, and according to their investor presentation Hadrian South is supposed to finish by about 2021. I’m not sure if that can be correct, but if so it’s production should be declining significantly soon. Also on Lucius, it’s biggest producing lease, really part of Hadrian North field, started showing a sudden water cut increase in May, and dropped about 8% production (for some reason this does not show up in BOEMs list of qualified fields, but it is definitely tied in to Lucius). The first lease on the Lucius field has been killed in about two years with water break through; it’s not clear what their plans are for it (this is Anadarko as well).

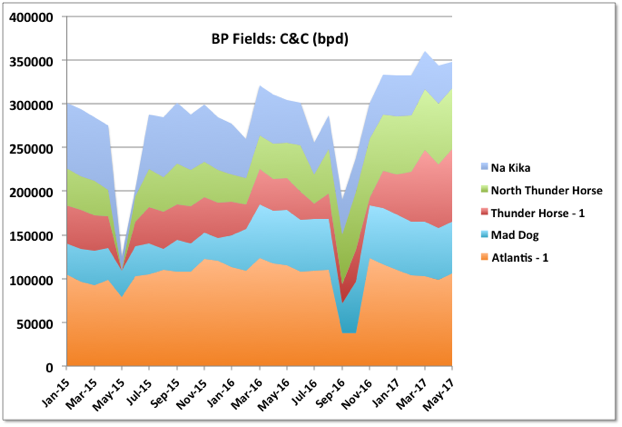

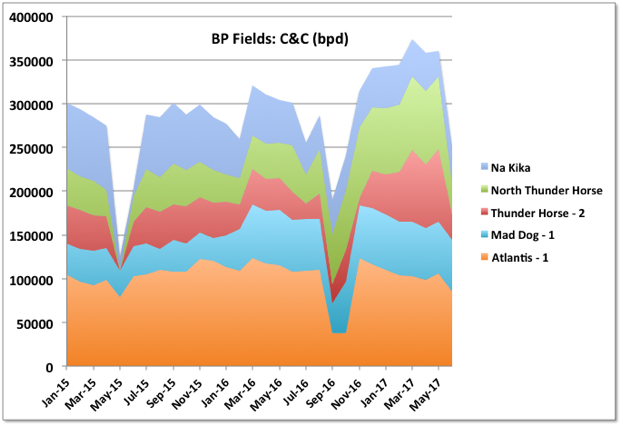

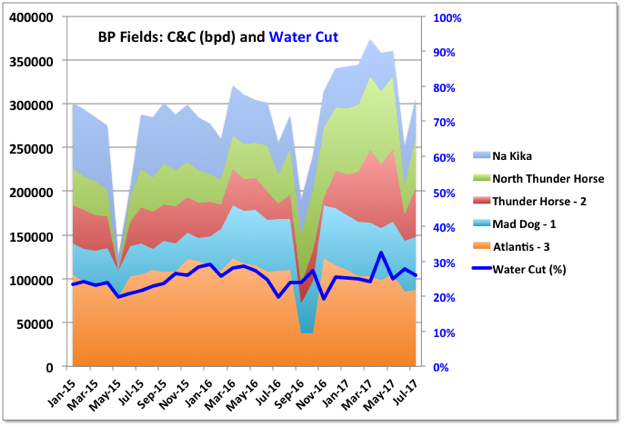

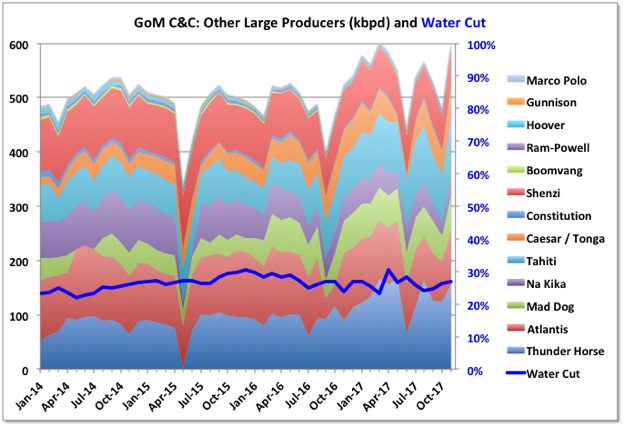

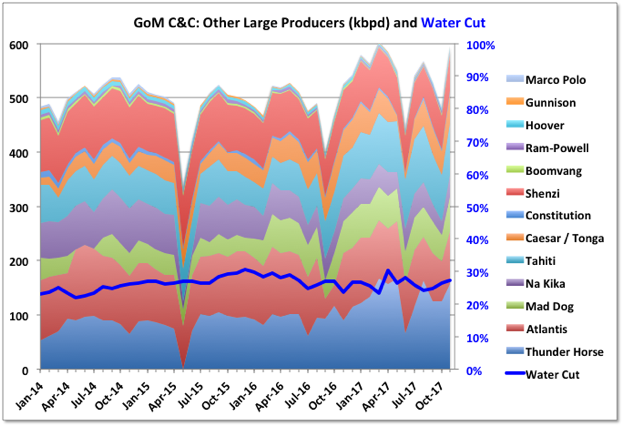

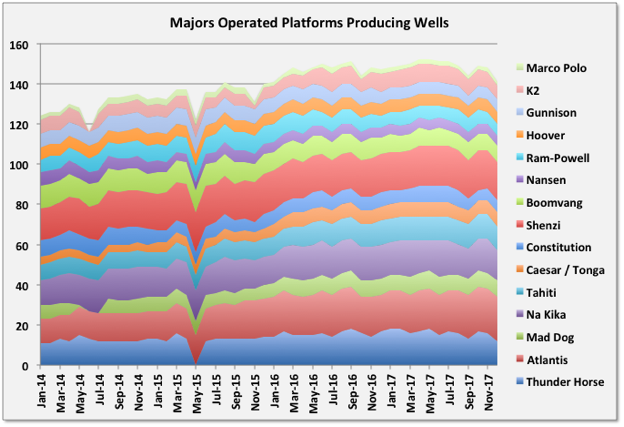

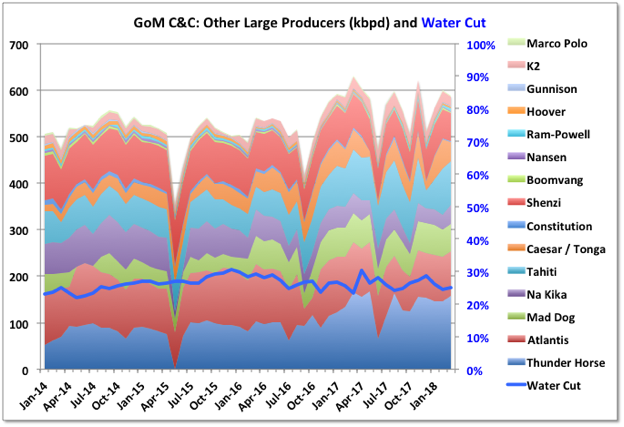

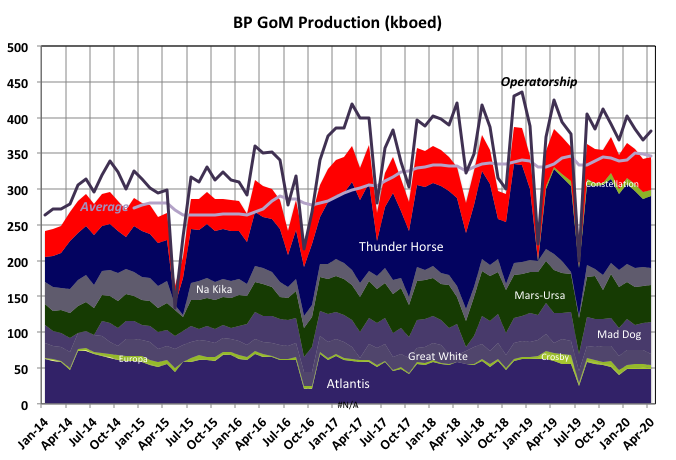

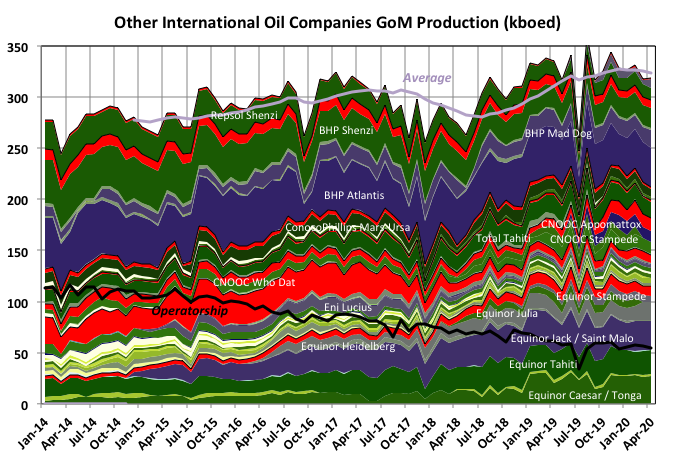

A couple of leases in Na Kika look like they have gone off line so production is down. Thunder Horse numbers were revised and now clearly show the impact from South Thunder Horse with about 35 kbpd increase. There have one rig still operating, but I think they will just maintain plateau now. Atlantis looks to be running about at nameplate capacity, so the coming North Atlantis development is likely only to be able to extend the plateau; there is one rig operating there now.

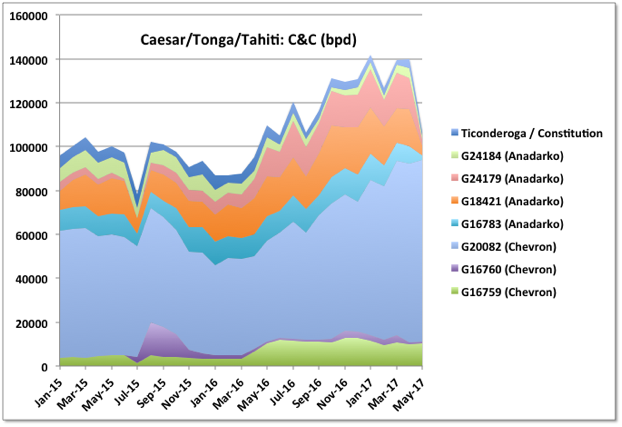

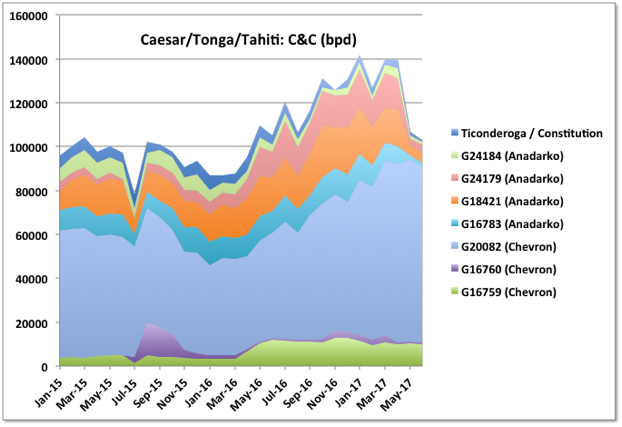

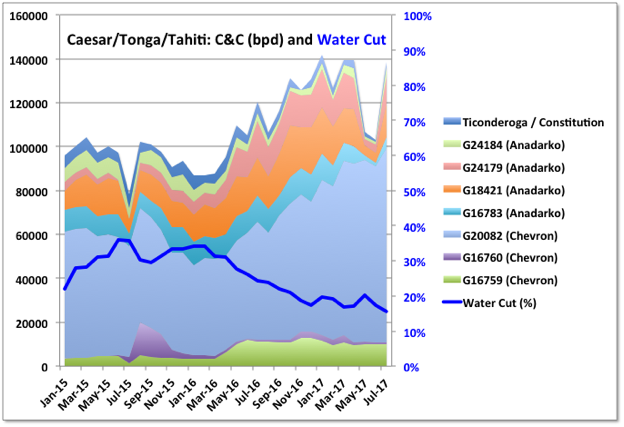

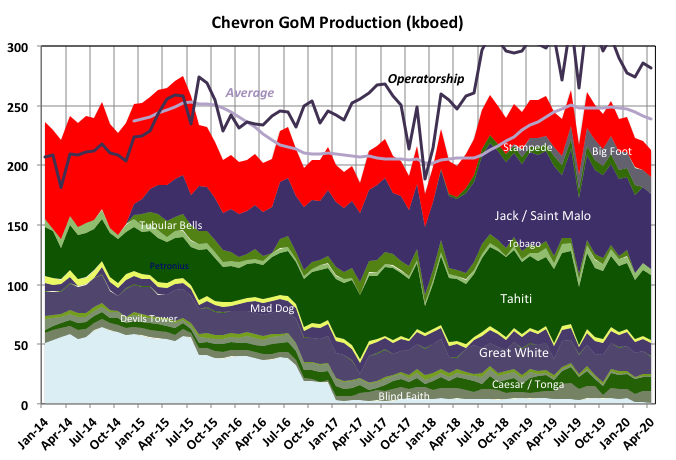

For the Caesar/Tonga/Tahiti fields the Anadarko facility (Constitution Spar) went off line taking off 40 kbpd production (Ticonderoga and Constitution fields go there too). The turn around was for 42 days so will reduce June figures too. The Constellation field is to be tied into the spar next year, the spar has nominal nameplate of 70 kbpd so another 25 or so (average) might be added to overall output.

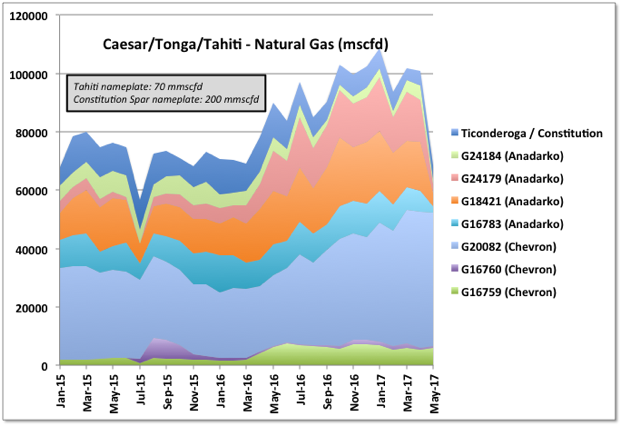

For the Chevron fields in these leases it looks like production is limited by the gas handling capacity on Tahiti platform, at 70 mmscfd, which is pretty low given it’s oil capacity of 125 kbpd.

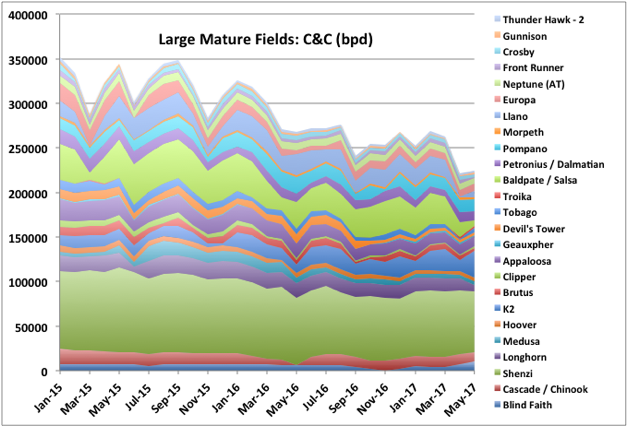

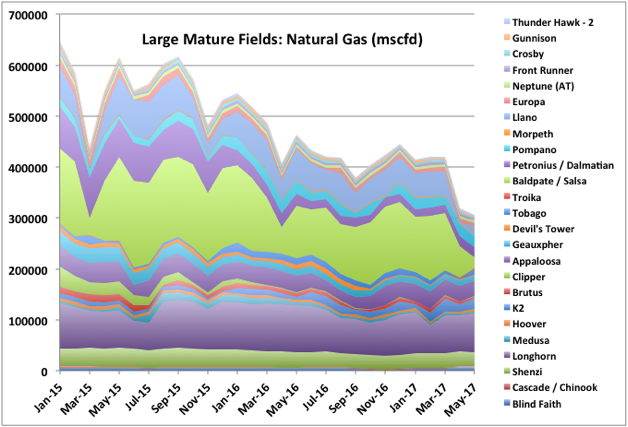

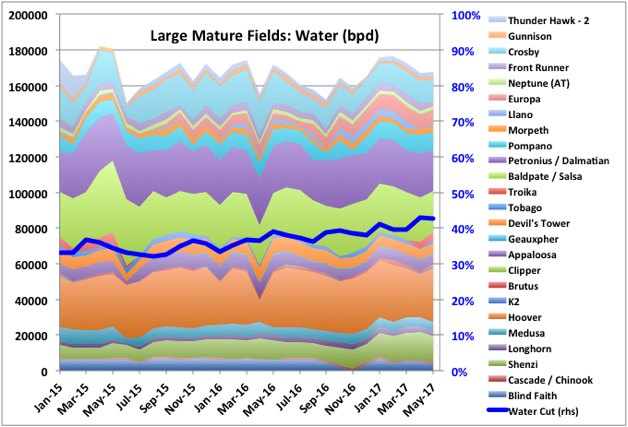

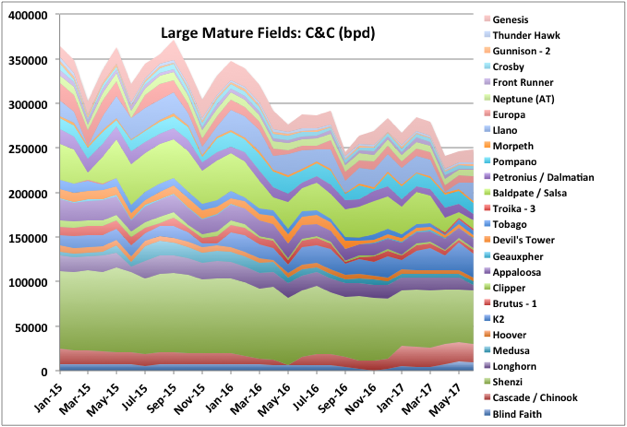

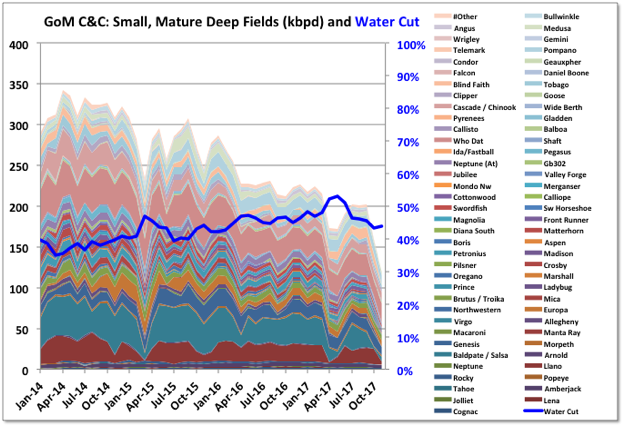

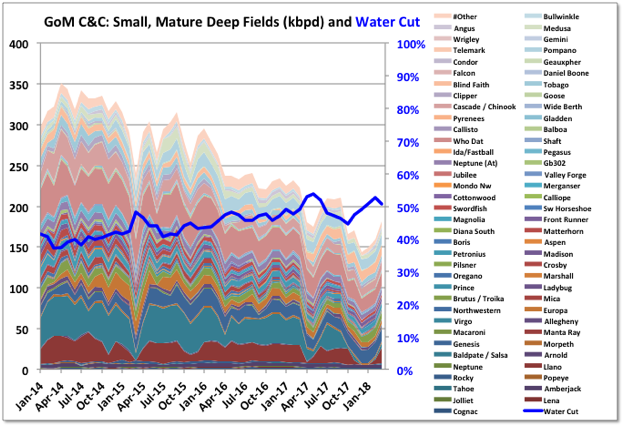

After a bit of a plateau from some brownfield work and new tie backs the decline in the larger mature fields looks like starting up again; the drop in gas is particularly noticeable, but is mostly due to Baldpate turn around. Overall water cut looks like it might be rising as well. Thunder Hawk has two new rigs operating, but I haven’t seen any announcement for new developments there. The smaller mature fields (not included in the charts) seem to be holding up quite well, I will try to get some individual lease data for these next month.

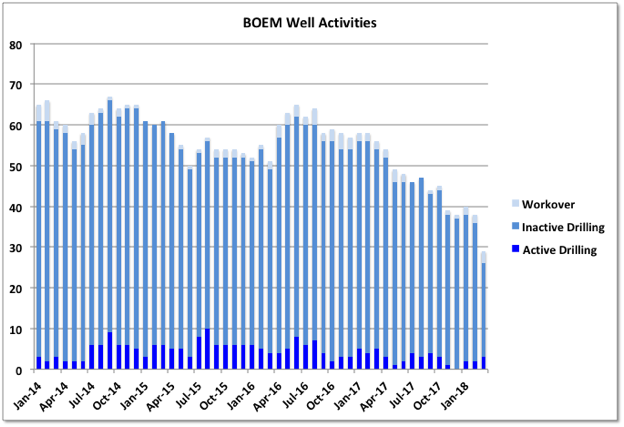

For the GoM activity report from the last week in July, there were 28 rigs drilling, twelve running tools and two in plug and abandon operation. I think the report can mean there is dual activity on a single well (e.g. wire line and drilling). Two rigs are predrilling on Stampede, one on Appomattox and one on Mad Dog II. For the newer fields there is development drilling on Lucius, Cardamom, Mars (two rigs), Stones, Julia, Jack / St. Malo, plus new wells for recently added or due production on Horn Mountain Deep and South Santa Cruz/Barataria. Atlantis also has a new rig, which may be for development of the Atlantis North discovery – it’s noticeable how any reasonable discovery is immediately fast tracked, the North Sea is similar. The Dorado field (operator Anadarko, discovery in 2014) is also being drilled; I think it is one of the last of wells for small fields (King, Dorado, Holstien Deep) being tied back to Marlin, there’s probably one more for King and a couple of others possible. Only Phobos has appraisal drilling.

Five rigs are drilling on unnamed fields, so presumably exploration – four of these are in Green Canyon, which means they are near field, and probably smaller, prospects; the other one is for Shell, in Walker Ridge, and probably a frontier wildcat. With all the predrilling on new fields, most new fields reaching plateau or decline periods, and few exploration wells (and fewer still in frontier regions) it seems likely that the drilling numbers will tend to decline over the next few years as unused well slots and tie back locations on the facilities are exhausted, even with an increase in oil price.

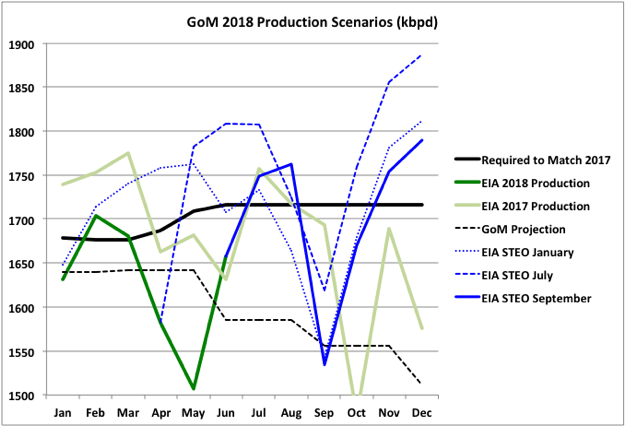

In the past few months as production rose the EIA STEO showed a new production forecast which had the same shape but was just raised to start on the new production number. They didn’t do the reverse as the production fell but instead kept the June STEO forecast with a single dip down for April. The August STEO, showing May data, is due next week.

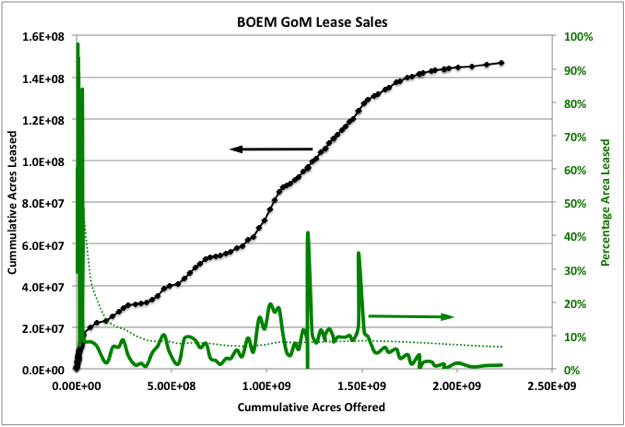

GoM Lease Sales

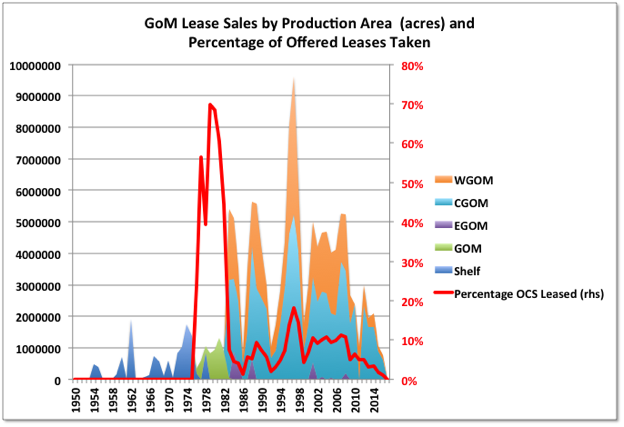

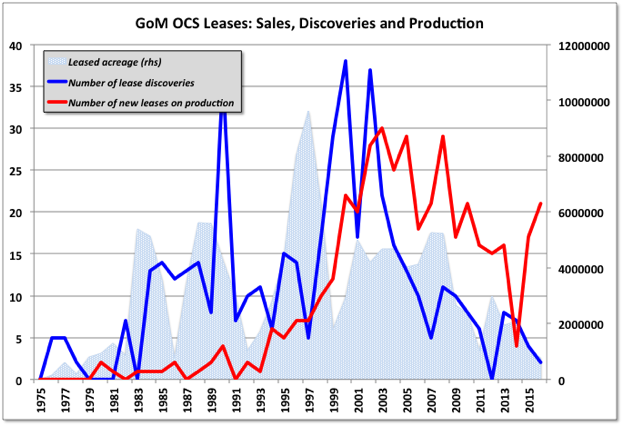

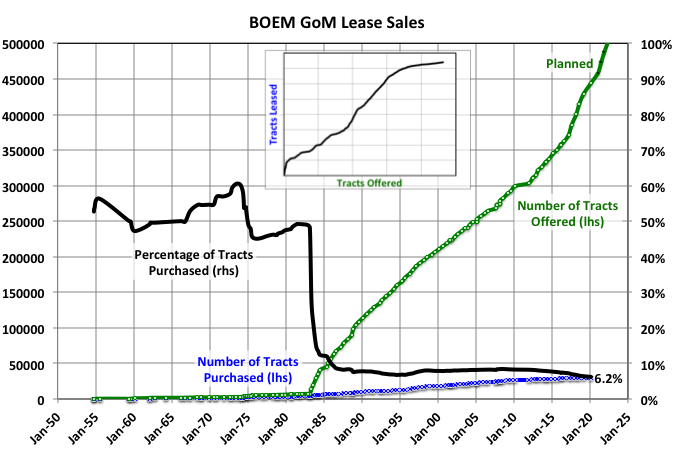

As further support that the current decline in exploration is not just a function of price, the chart below shows the acreage of GoM leases that have been successfully auctioned, plus the percentage of offerings that were taken up (charts are stacked according to BOEM designated production areas to the give total). The numbers before about 1976 are listed against states (FL, LA, TX) and I think are inshore shallow leases, although it might be they just changed naming convention. After about 1990 areas were split from just GOM to east, central and west. The percentage bought calculation only considers the area auctioned after 1990. It is marked how the amount bought and the percentage bought both peaked and rapidly dropped off, even in the high price years through to 2014. However there were obvious impacts from earlier price collapses in the late nineties and 2008.

It’s possible to read too much into these charts but generally it looks like, on average, discoveries follow three or four years behind the lease sales and production about the same length after that. But the recent production rise isn’t in that pattern – maybe disrupted by the 2008 recession and 2010 drilling hiatus, or maybe the high oil prices after 2011 allowed some difficult and expensive long term discoveries to become commercial.

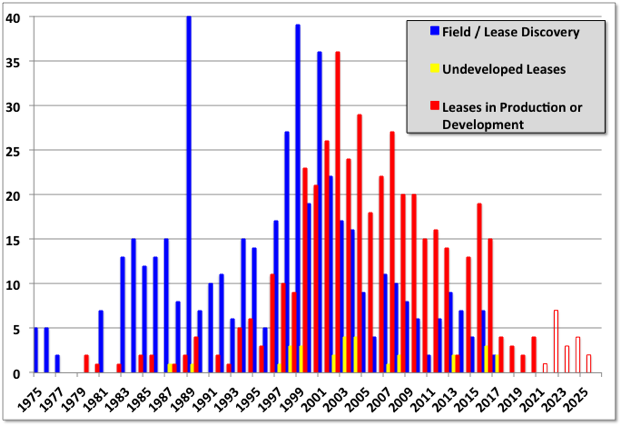

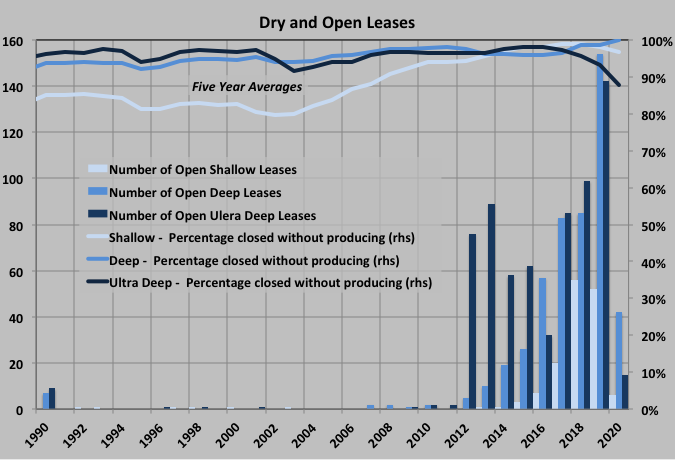

The number of open, undeveloped leases is relatively few, and declining. The chart below shows the number of leases discovered (and not terminated without development), producing or in development, and those still undeveloped. The open bars show my guesses for some larger fields that seem likely to be approved soon (e.g. Vito, Anchor). Most of the undeveloped leases (in yellow) are associated with existing, fairly recent, fields on production (e.g. St. Malo, Tubular Bells( and are likely to be poorer wells, waiting on surface facility capacity to become available before being tied in. There are two new field discoveries this year: Mormont and Khaleesi, by LLOG in Green Canyon (they have switched from Animal House to Game of Thrones naming convention) and are likely to be smaller reserves similar to their Delta House developments.

There is one area that might be expanding: deep shelf pre-salt. These are deep or ultra-deep wells but in shallow water (this is a rare combination and hence one problem is that there aren’t many rigs – jack-ups – that are suitable). W&T brought on Mahogany field this year, in an already producing lease (one well at 5000 boed with up to three others due, although the production data suggests it wasn’t as great as expected) and there may be more to come. The production is high pressure and high temperature, and in places can be too high for the available technology or commercial development, and mostly gas prone.

Production for June by BOEM was 1631 kbpd and by EIA 1636, compared with 1673 and 1659 kbpd, respectively, in May. The decline was mostly from Thunder Horse going offline and Constitution staying offline. Hurricane Cindy didn’t seem to have much of an impact, things will be different for the impact of Harvey on August figures.

Even with the two offline facilities coming back July numbers will struggle to beat those for March, and after that the depletion declines and hurricane disruptions take over. Note that the “others” area includes any assumptions BOEM has made to allow for missing data, which is quite a lot this month.

The combined new fields added from late 2014 are holding a plateau with South Santa Cruz and Barataria fields added and a new lease for Marmalard starting (adding about 20 kbpd combined). Stones also had a better month and achieved 70% of nameplate capacity. It’s interesting that five leases have come on line and then have effectively been killed off in this thirty month period: Amethyst (a small gas field that died after sputtering along for about six months, and not shown as the flow was so small), one lease in Lucius, Kodiak, one lease in Caesar/Tonga/Tahiti, and one in Rigel. Dalmatian South production fell immediately after start-up and was offline for a couple of months but came back in June (there are plans for subsea pumping to be installed but I don’t now the present status).

The big drops have been for BP, with Thunder Horse off line for part of June, and for Anadarko with the Constitution shut down extending into a second month (I think a bit longer than was planned).

Mature deepwater fields continue a general decline. Note for all fields there is some missing data for June and even in May – I have assumed production remains constant from the previous given month’s numbers in each case. For some reason Hess’s Tubular Bells has no reported figures for eight months now.

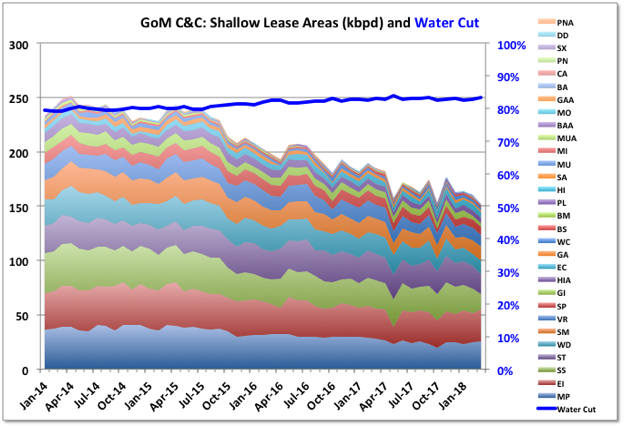

Shallow Fields

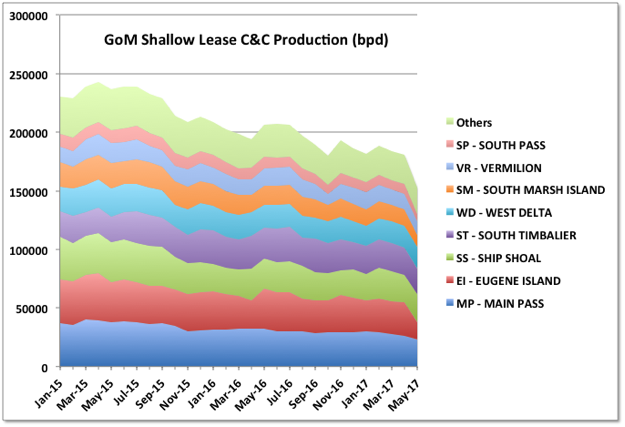

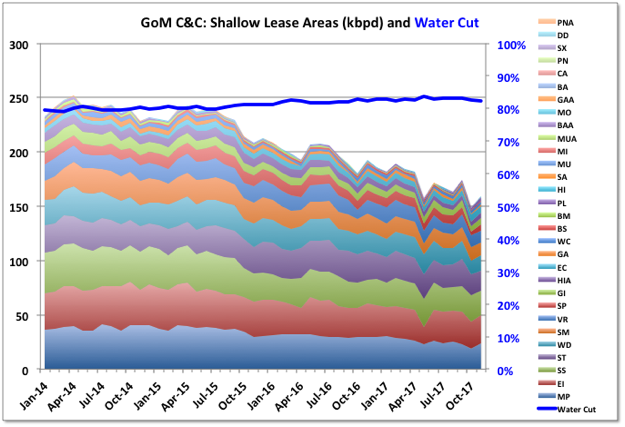

The shallow fields in the GoM are in steady decline for both oil and gas, but different leases are more oil and gas prone.

Production Breakdown

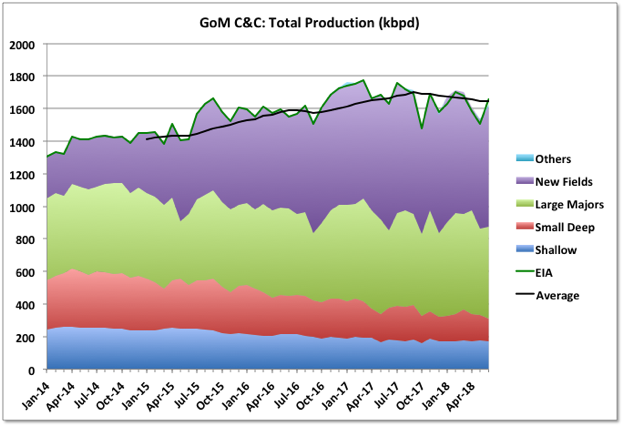

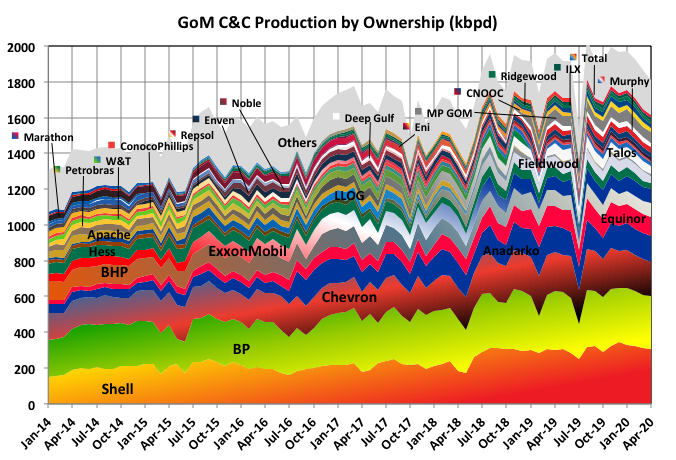

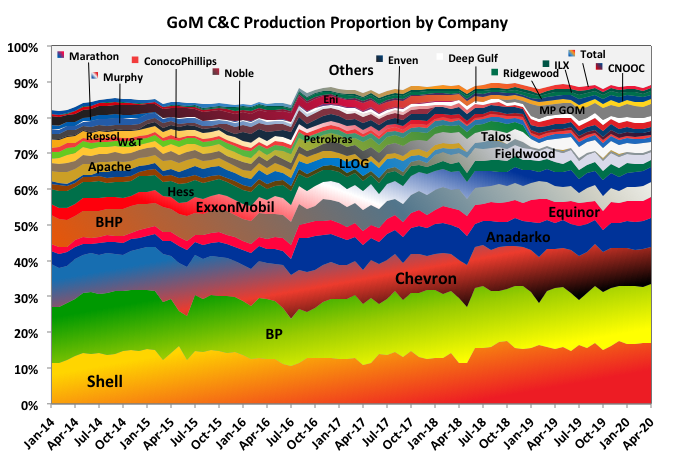

These charts show breakdown of production by company – most oil comes from four companies: Shell, BP, Chevron (including Union Oil) and Anadarko (their historical numbers include those for Freeport McMoRan, which they bought last year) – and by depth, which doesn’t tell me much, except maybe that ultra-deep hasn’t delivered as much as was once expected. Note these charts only go to May as June has a lot of missing data for the shallow leases (and some for May too I think, but it all comes from well numbers and there are too many to check).

Lease Expiry

BOEM provide data of when undeveloped leases have expired or will expire. There has been only one so far this year (Kaskida). However there are a lot due over the next few years, as shown below. Presumably they can be extended, though at some cost, but this may indicate a lot of development decisions (for both greenfield and browfield work) need to be made in the coming couple of years. Some of the big ones due this year are Shenandoah, North Platte and Yucatan; next year and 2019 there are a couple each in Rigel and La Femme, plus Anchor, Leon, Gibson and Samurai, and overall another six or so associated with older producing fields (i.e. that would require tie-backs or outreach drilling).

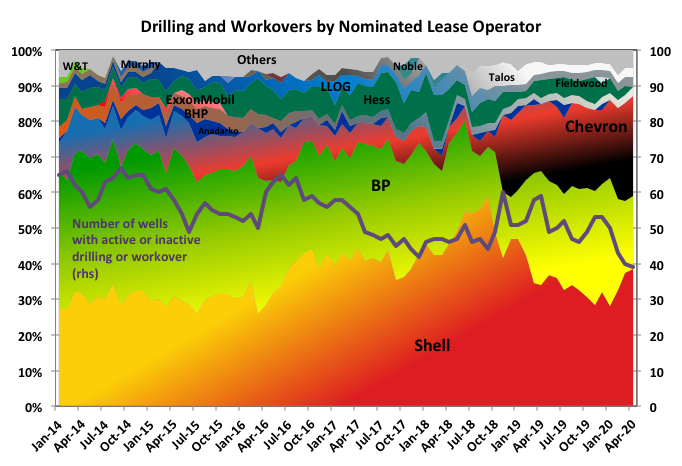

Drilling and Workovers

There are thirty rigs listed with drilling operations in the BOEM deepwater activity for 29th August, plus sixteen workover operations (in any of the charts if there is a number after a name it shows the number of well operations listed against that field). Six rigs have no field listed so are presumably wildcats. There don’t seem to be any appraisal wells in progress. Also any impacts from Hurricane Harvey aren’t apparent (the rigs that were abandoned were mostly jack-ups in shallow water so wouldn’t be included).

Off Topic Finish

This is a house designed by Frank Lloyd Wright for Marilyn Monroe and Arthur Miller but never built. It’s computer generated from his original design drawings, although the second floor private quarters are missing. At the site below you can take a walk though the rendering. Miller didn’t like it and they couldn’t afford it.

I don’t know much about architecture, and I’m not sure if I even know what I like, but Frank Lloyd Wright’s work is unique, he was not much of a fan of right angles. A lot of his designs never got built (as with many architects I expect), but like this many have been rendered in graphics packages, often as an example of their capabilities. He designed a civic centre and transit building for LA, which looks a bit like the Tyrell building from Blade Runner (which, amazingly, was set in 2019 – that seemed a long way away when the film first came out), though I don’t know if it was the model for it.

GoM C&C production for July by BOEM was 1746 kbpd and by EIA 1761, compared with, respectively, 1631 and 1634 kbpd (corrected) in June. The EIA number is a new peak, the BOEM one is still 24 kbpd short of their March numbers. The growth was from Thunder Horse (partially), Constitution and Baldpate/Salsa (which is mostly gas) coming back on-line, plus continued ramp-up in Stones and Marmalard.

C&C Production Details

For new fields added since late 2014, data for Tubular Bell’s, which has not been available since late 2016, has been updated and shows a growth of about 14 kbpd in that period, hence there is now a slight continuing rise shown in new lease production over the past six months, rather than the previous plateau; Tubular Bells looks like it is now on plateau, about 40% below it’s nameplate, and there is no current drilling.

Dalmatian North (online in March 2014) and Dalmatian South (online in December 2015) are small oil fields, which are not performing very well and might well go off line soon. At the moment it looks like their production is cycled every three or four months. Subsea pumping is due to be installed for them in late 2018.

Heidelberg and Marmalard look to be about at their expected rate (Heidelberg is only about 50% of facility nameplate but I think more would have to come from additional tie-backs and I don’t see any drilling for that at the moment). Julia is the one reasonably sized recent addition that is still below nameplate and has current drilling, so could add another 15 kbpd, but with rapid decline in the first year based on the first well (it has subsea pumping installed but I don’t know how much that improves things). Stones is just about at expected capacity after what looks like quite a difficult start-up over about twelve months, but sometimes facilities can achieve higher rates early on, though I don’t know how long the approval process takes in the GoM to go higher.

The water cut on the new fields looks like it’s starting to creep up, a possible sign that the production is plateauing. Of all the new leases started since 2015 only one in Tubular Bells and three in Great White have pressure support from water injection wells (though Jack has provision to add it later). I think the other leases mostly rely on pressure depletion, with some partial aquifer drive or compaction drive support, which means that unless they are limited by surface facilities and have to be choked backed, and I don’t think many are as the facilities are generally operating below nameplate capacity, they will continuously decline unless new production wells are added. There are some older leases within the fields shown also with water injection, for Holstein, Mars-Ursa and King, but overall most of the production shown is likely now to start to show increasing decline rates as development drilling winds down, and as is already evident in a lot of the smaller fields.

Thunder Horse was back online for most of July following a prolonged turnaround. There is still drilling there so there may be some more production to come from South Thunder Horse. Atlantis also has a lot of activity, possibly for North Atlantis start-up next year.

The Constitution Spar also came back on-line after a long turn around. I’m not sure if there is any more to some in the Chevron leases produced through Tahiti, but there has been significant growth there over the past year (it was started in 2009 and a more typical production facility would be coming of plateau about now).

The deep mature fields continue a general decline at 15 to 20% y-o-y. The water cut has declined a bit, possibly as some of the older wells water out and are shut in.

The shallow wells show steady decline, note however that there is missing data for July, and probably a bit in June.

Hurricanes and Other Unplanned Outages

Thunder Horse was shut down and fully evacuated following a power failure mid September. That is a pretty major upset and shouldn’t happen (it would, in theory, require at least two independent failures), and would take a few days to find and correct the problem and get permission to restart. I wouldn’t be surprised if it was related to previous evacuations for hurricanes. Thunder Horse produces about 180 kbpd.

The estimates for hurricane related lost production were 84 kbpd (average over the month) for August and 60 kbpd for September – the Thunder Horse electrical outage might add another 20 kbpd to that. There may be some natural decline to add as well. On the other hand Thunder Horse was not at full capacity in the July figures, so could add another 40 kbpd when it finally gets there.

For natural decline rates the mature deep-water fields are dropping just under 80 kbpd per year and shallow fields about 40 kbpd per year, so maybe 10 kbpd per month overall. The new fields and the BP and Tahiti related fields also have natural decline on many of their wells but it is being covered by ramp-up of new fields and in-fill development wells. However both those sources are starting to ease off so the overall decline rate will start to climb, eventually to as high as 20 to 25% based on R/P numbers.

Overall then, there is likely to be a slight decline seen in the next couple of reports for August and September, but not as dramatic as the hurricane news might have suggested. However the impact from Nate in October, plus a bit from the shut-ins on Delta House following the subsea pipe failure and subsequent leak, will be more significant, around 300 kbpd on average, and with some knock-on impact into November and later because of the drilling rig outages and depending on how much of, and for how long Delta House production is lost. I will probably not put together another update until the November figures come out as it will be difficult to tell what is happening on individual fields given the various shutdown and restart disruptions, but it will be interesting to see what EIA do with their STEO predictions.

Natural Gas Production

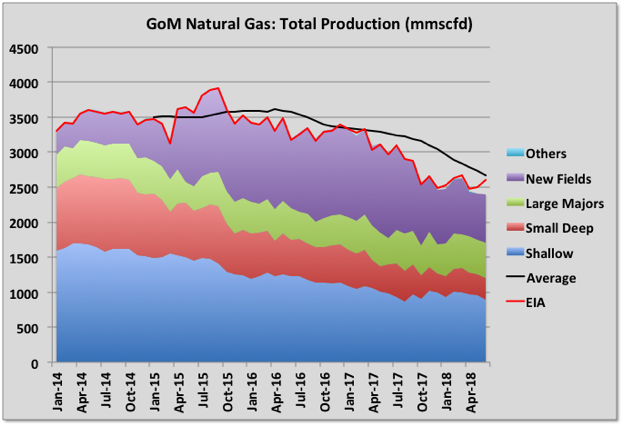

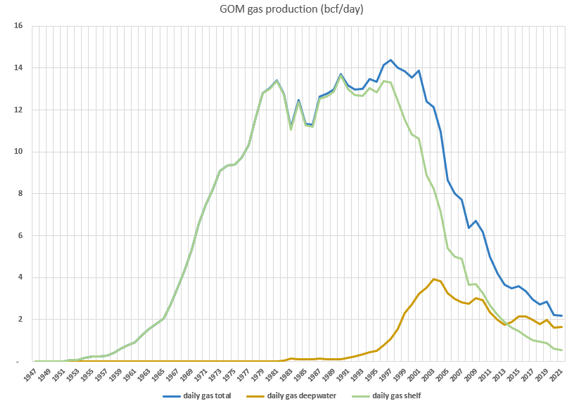

Most gas production is associated gas and is in slow decline from a local peak in 2015 (note this was about 80% lower than the main peak in the 90’s when there were still large gas fields in operation). Most gas comes from the main deep water areas: GB – Garden Banks, GC – Green Canyon, MC – Mississippi Canyon, and KC – Keathley Canyon. The thin lines on the top of the chart are mostly shallow lease areas and are in steep decline at over 20% y-o-y. As oil decline picks up so will the overall gas decline.

The new fields gas production is now showing clear signs of decline, mainly coming from Hadrian South (the only recent, largish natural gas field that’s come on line, but with R/P of only a couple of years based on remaining reserves from January 2016 at nameplate capacity, so bound to decline fast at some time).

Recent Drilling and Leasing Activity

By the BSEE report for the last week of September there were 41 GoM well related activities in progress. Only two unnamed wells, indicating wildcats or appraisal, were being drilled: one, by BHP is Scimitar in GC 392 (which follows an announced oil show in Wilding-2 in a nearby block – Wilding-1 had a mechanical failure and had to be re-drilled); and one by Shell in WR 376. There are two P&A operations, eleven rigs running tools through wireline or coiled tubing, and twenty-nine active drilling rigs (including three predrilling for Stampede, Mad Dog II and Appomattox).

Total and Chevron have entered into an agreement to drill eight near field exploration wells around the Anchor and Appomatox discoveries. The first was spudded in July on the Ballymore prospect (MC 607), which is listed against the East Anstey field, so may not count as a true wildcat.

There were no new discoveries, start-ups or lease qualifications in September. One producing lease expired: Dalmatian, a small gas field started in March 2014; it had produced 30bcf and 0.15 mmbbls.

Recent Business Decisions

There has been one definite FID decision in September for Buckskin. That will be tied in to Lucius, which would suggest there are no expectations that the lease there that was killed off in a couple of years with high water cut will be recovering. Buckskin will use two 8” flowlines. I haven’t seen expected production but I’d guess around 20 kbpd, due in late 2019 for LLOG (after Chevron, Maersk and Repsol have all pulled out as operator). At one time a large, stand-alone development combined with Moccasin (now dropped as an active lease) was expected. It is deep-water, high pressure but uses riser base gas lift, which suggests a tight reservoir, and probably fast decline with depletion drive.

LLOG also announced tie-backs on a number of other small developments that are due in mid to late 2018 (I don’t know if these are formal FIDs yet, LLOG is a private company so doesn’t follow quite the same requirements as publicly listed ones, but these projects do have other partners who would need to agree): Clairborne, two wells tied to Coelacanth; Red Zinger, one well tied back to Delta House; Crown and Anchor, two wells tied back to Marlin; and La Femme / Blue Wing Olive (apparently a type of fly used in fishing), three wells tied back to Delta House. These will all be fairly small flows, I’d guess totaling around 45 to 60 kbpd nameplate and likely quite fast declining. All the wells to be tied back have already been drilled as exploration or appraisal.

In terms of net additional production there is little or no spare capacity on Delta House (before the leak it was at an average of 90 kbpd and rising on a nameplate of 100, and it is designed with minimum on-line sparing so availability would be low), so the additions there imply the existing production is expected to be declining: the sister platform, Who Dat, showed quite fast decline after three years, which is about how old the Delta House fields will be mid 2018. There is quite fast decline on a couple of the fields on Marlin already, but there is existing spare capacity. Coelacanth is only at 11 kbpd on a nameplate of 30 so there’s plenty of capacity but I think Claiborne is small even by recent standards.

On the other hand Anadarko, who had continued to be fairly active in exploration and development offshore, have signaled that they are going to use their cash flow for share buyback rather than seeking more growth (the Freeport MacMoran purchase last year may not be turning out to be such a great idea). With Anadarko cutting back LLOG is the most active player for developments at the moment though the recent pipe failure and shut down at the LLOG operated Delta House may delay things.

With these announcements there are now only five named discovered fields in the GoM that are not being produced or have fairly firm production plans, if not quite at FID yet – two small ones discovered this year, the other three also fairly small. There are a few other likely discoveries that have not been fully appraised and some undeveloped leases attached to existing fields.

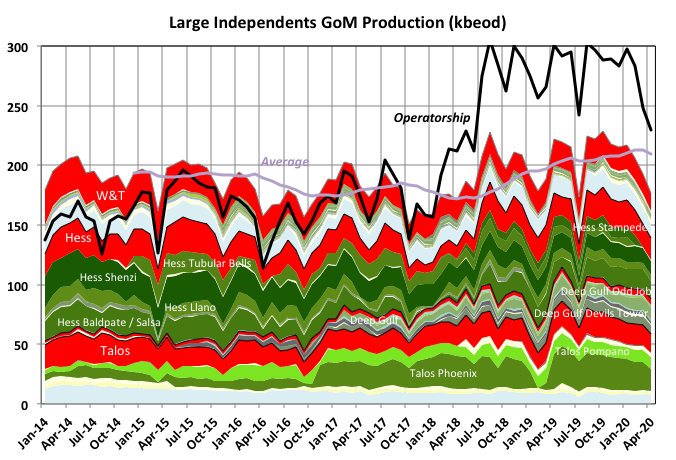

Shenzi (shown as the largest producer of the mature fields in the chart above) is operated by BHP. Some activist investors there are trying to get the company to pull out of oil and gas completely. Shenzi is not a typical asset to sell, as it’s a fairly major producer in mid life. BHP is the fifth largest producer in the Gulf.

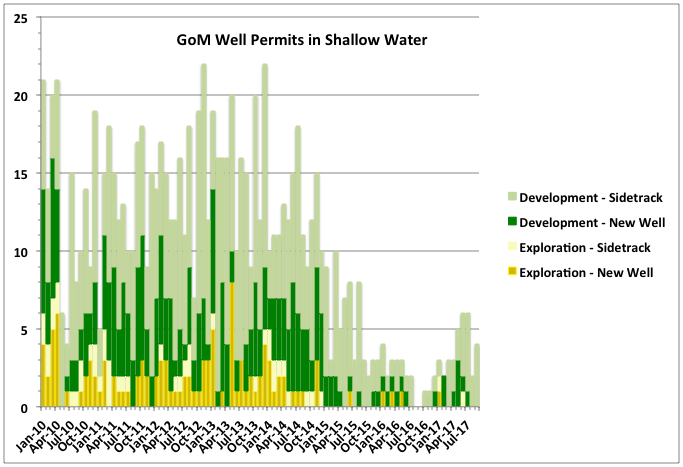

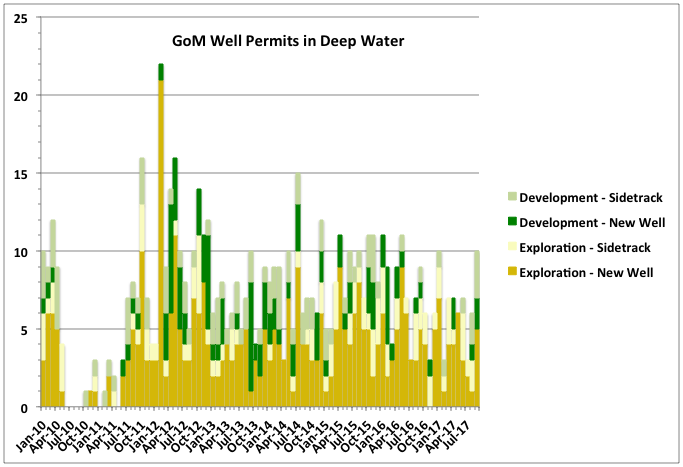

Well Permits

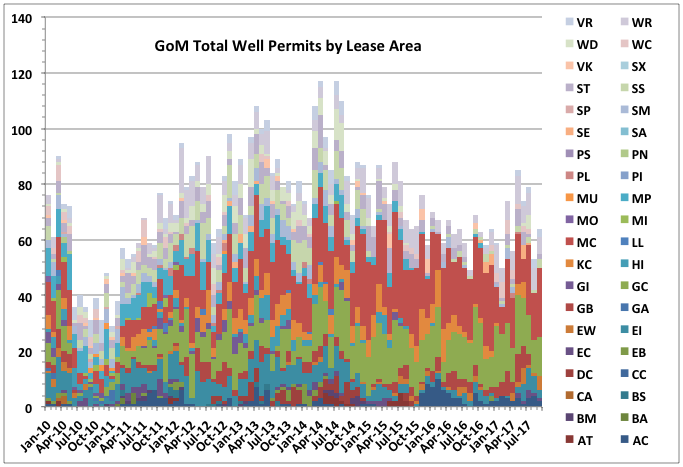

As an indicator of longer-term production trends well permit numbers come after lease auction bids. Exploration wells indicate possible discovery rates and later FIDs and development well numbers indicate expected production in the nearer term. BOEM has extensive and up to date permit records. The charts below show numbers from 2010, with the hiatus in drilling following the Deepwater Horizon accident clear in each. They all show oil, gas or injection well numbers as I couldn’t find anywhere that these are differentiated, however most will be related to oil fields. For the first two charts I’ve only included new wells and sidetracks – i.e. wells with newly identified targets – and excluded amendments and bypass wells. The exploration numbers include appraisal wells.

Shallow exploration has pretty much finished now, and development wells are also tailing off, with recent ones being sidetracks of older wells. Sidetracks mean well slots, and maybe wellheads, on exhausted wells can be reused for new targets without requiring new facilities (I’d guess there are now no free well slots on any of the older, shallow platforms).

Deep water exploration and development numbers are also declining but relatively slowly. However with recent low lease sales, a big drop in new projects coming on line and some of these development wells being predrilled for the few coming projects there could be a sudden drop next year (pace other influences, e.g. a sudden price rise might prompt more in-fill and exploration drilling).

For all permits, including amendments, numbers are steadier but still dropping slowly. Most of the action is in the four main deep water lease areas: MC, GC, GB and KC (see names above).

Off Topic Finish

EVs obviously have a lot of longer term advantages but whatever else they may do they don’t sound like classic supercharged muscle cars:

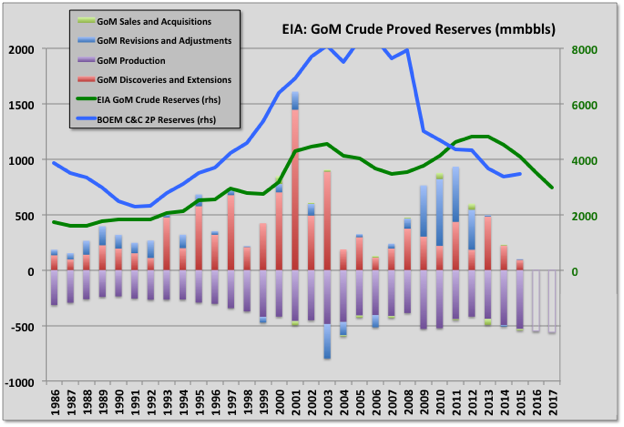

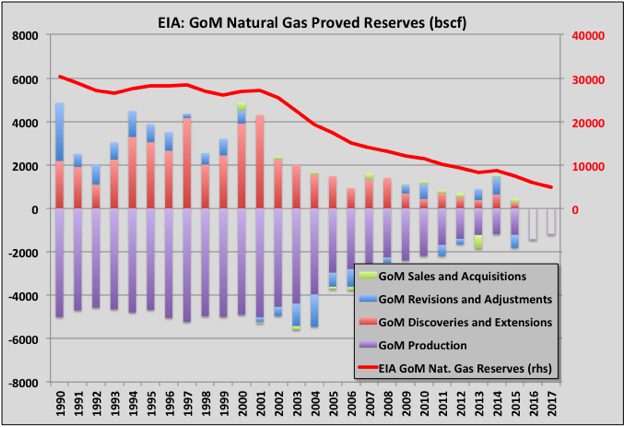

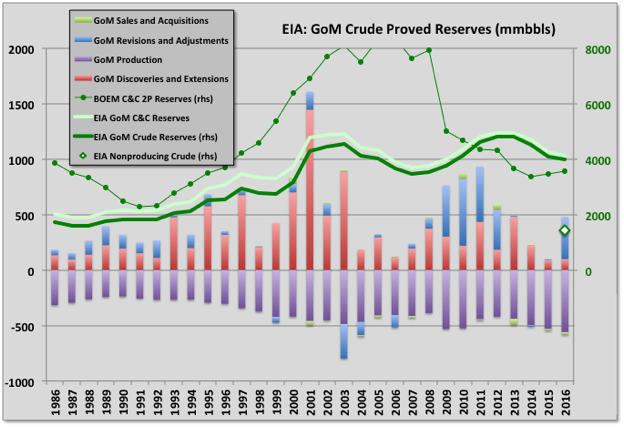

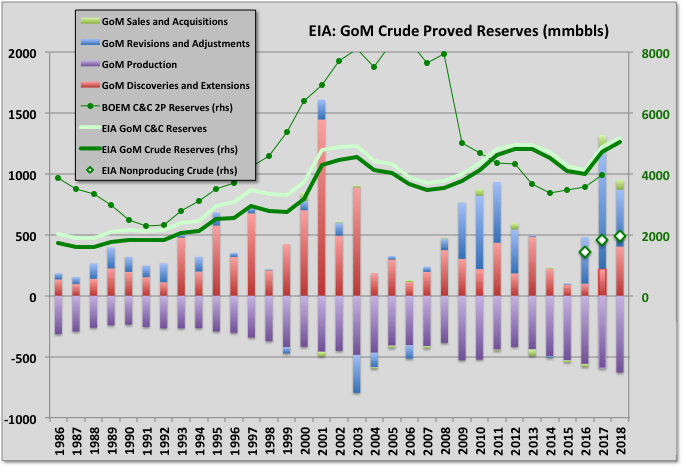

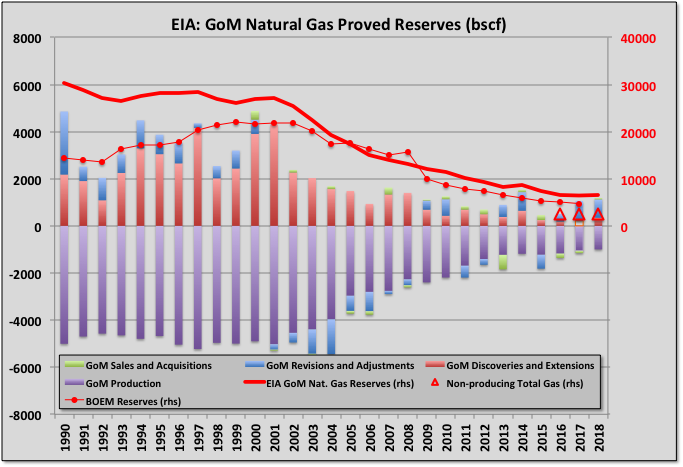

EIA provides estimates of proved reserves based on information from the E&Ps on form EIA-23 for crude only, and also shows the categories for changes (discoveries, production, revisions etc.). This data with updates for 2016 has been due since November but so far has been twice delayed. BOEM make their own estimates for 2P (i.e. proved and probable) based on strict adherence to SEC/SPE rules (i.e. the reserve must be on production or be expected to be produced within five years). I think this usually comes out in May. In the absence of the latest EIA numbers I’ve presented the 2015 numbers with adjustments for subsequent production. There will be revisions and additional discoveries to include once the actual data is available though I think fairly small, especially for gas, but it will be interesting to see.

Despite excluding probable reserves and counting crude only, the EIA estimates have recently exceeded those from BOEM. It looks like a lot of the probable reserves were converted to proved through positive revisions in the period 2008 to 2011; i.e. possibly due to some price increases then, but also immediately following the SEC rule changes to exclude reserves without firm development plans, which may or may not be coincidental: the E&Ps may be less strict on applying the SEC/SPE rule, which they are allowed to do for large, long term projects. The BOEM estimates are pretty much flat over recent years as additions (which then become backdated “discoveries”) from new projects going through FID balance production, whereas EIA estimates are declining with revisions recently zero to negative.

Sales and acquisitions mostly balance out, sometimes with a year or so lag, though overall slightly positive, which I guess means the purchasers are able to get a bit more from the fields than the sellers. There are few extensions to conventional fields (unlike LTO where they are the largest positive factor) and discoveries have trended down significantly over the last three or four years (this would probably have happened a couple of years earlier but for the drilling hiatus caused by the Deep Horizon accident).

C&C Production

For November the production losses from Hurricane Nate have been recovered but more than 100 kbpd streamday was lost because of the subsea connector failure on LLOG Delta House Rigel template and the Shell Enchilada gas line failure. Total oil by BOEM was 1675 kbpd (up 211 kbpd m-o-m but down 16 kbpd y-o-y) and by EIA 1666 kbpd (up 209 kbpd from October, but down 21 kbpd y-o-y). Note that several leases did not report November numbers so I have had to estimate production based on data from the months before the hurricanes started to have influence.

New fields production has peaked for the time being, even allowing for the offline fields. Stampede might give it another boost once it comes on-line soon. The smaller additions are generally in decline, but there has been some in-fill additions for Horn Mountain, Holstein and Phoenix.

The large platforms, and Mars-Ursa should be considered with the ones listed, are holding and increasing production the best. I don’t know how much more there is to come, but certainly Tahiti and Atlantis have large brownfield developments in progress. The larger ones shown are around ten years old, which would normally be around the end of a plateau period, but equally they tend to have a lot of excess processing capacity. If nothing else some of them must be due for major turn-arounds in the next couple of years, which would take about as much production out for a year as Nate did.

The smaller, mature fields took a hit with Enchilada offline, but maybe not as big as might be expected given their continuing steep decline.

Shallow fields continue to decline. There was some headline news concerning Byron drilling the South Marsh Island 71 block, but it only has about 4,500 bpd capacity.

Recent News and Activity

The Enchilada pipeline is still offline with no date for restart published yet, which is keeping about 75 kbpd oil production offline from Baldpate, Salsa, Cardamom and Magnolia since early November. The workers injured in the incident have started proceedings against Shell for compensation due to safety failings. All these fields were in fairly steep decline so the production, and therefore revenue and interest, is only lost while they are offline rather than being deferred several years, as would be the case for a system on plateau. The subsea failure on the Rigel manifold feeding Delta House has resulted in Rigel, Otis and Son of Bluto 2 being off line for most of October and all of November (about 40 kbpd capacity). I have seen no news that this has been repaired. Without these two major unplanned outages November would just about have beaten the March record for production.

Anadarko relinquished the Phobos lease after poor appraisal well results. It had been the only qualified lease in the far south Sigsbee Escarpment lease area and was being planned as a long tie-back to Lucius.

Maersk Drilling has lain off workers that had been working on the Maersk Viking for ExxonMobil’s Julia field, which seems to have finished ramp-up although there had been plans for a phase II there. It had been in quite steep decline but there has been about 6,000 bpd increase in the flow over the last two months and it may be near a new peak. Stones drilling has also stopped, it has a nameplate of 40 kbpd but has only so far exceeded 30 for one month. Heidelberg drilling, too, has now stopped and it has achieved about 40 kbpd of a nameplate of 70 kbpd; phase II is due in 2021.

Tornado II started production in mid December at about 10 kbpd oil. Combined flow for Tornado/Phoenix is currently reported at about 21 kbpd oil, or net 8,000 bpd up on the average with Tornado I alone. There’s also been a big increase in the Horn Mountain lease, which has gone from less than 10 kbpd and declining in May, to now over 32 kbpd.

Two non-quantified discoveries have been announced as variously “major”, “significant” and “amongst our biggest”: Whale for Shell/Chevron, which does sound pretty big and is near the Perdido platform, and Ballymore for Chevron/Total, which is near Blind Faith. I suspect both will be tie-backs as the reason for concentrating on near field exploration was to save money on subsequent developments. Perdido has 100 kbpd nameplate and currently produces 66 kbpd, and Blind Faith has 60 kbpd with over 37 kbpd capacity available, and rising. Appraisal drilling is continuing on both, and that hasn’t always been as great as the initial announcements (e.g. Kaskida, Shenendoah and, recently, Phobos). I’m not certain, but think they both may count against last year’s discoveries and the announcements have been delayed to be immediately concurrent with the 2017 financial statements.

Wood Mackenzie was reported as giving predicted 2018 GoM deep-water production of 1935 kboepd, a new record. I think this is an average rather than a peak or exit rate, but I couldn’t find for sure. Note this is oil and gas (reported as including 80%, I think C&C only, but could be total liquids) and doesn’t include shallow water, which may be below 500’ (common industry limit) or 1000’ (BOEM limit), the report didn’t say. I don’t know why it was made so complicated, probably so they can declare a record of some kind that would help to try and sell the full report.

Currently (early February) there are forty-nine deep-water well related operations in progress reported by BSEE. Thirty-four are drilling related, with five pre-drilling for future projects and four on unnamed fields (so wildcats or appraisals). Of the fifteen running tools one is for P&A on Tick, which is fairly shallow water. Numbers in brackets on the production charts show the number of listed activities for each field. There is no current indication that the increased oil price is leading to increased drilling and the Baker Hughes count of active rigs has actually fallen slightly recently, though there may be signs of an uptick in non near field wildcats, but probably still early to say.

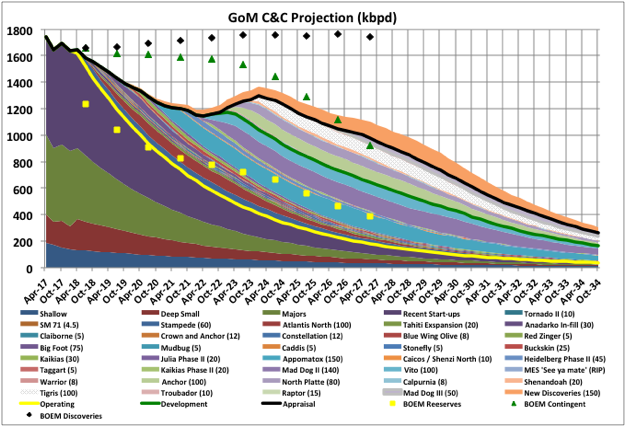

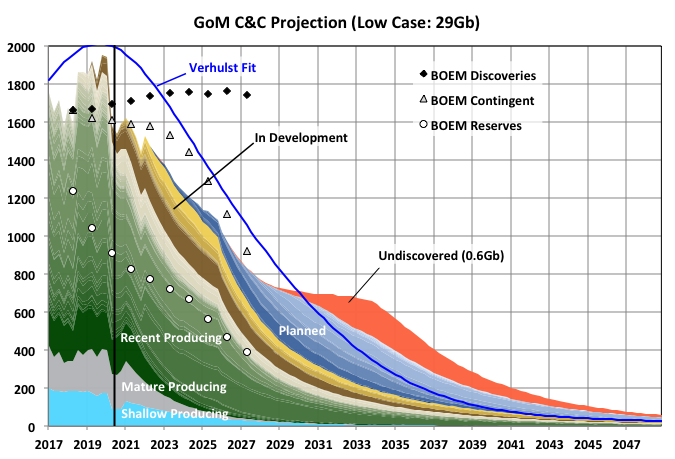

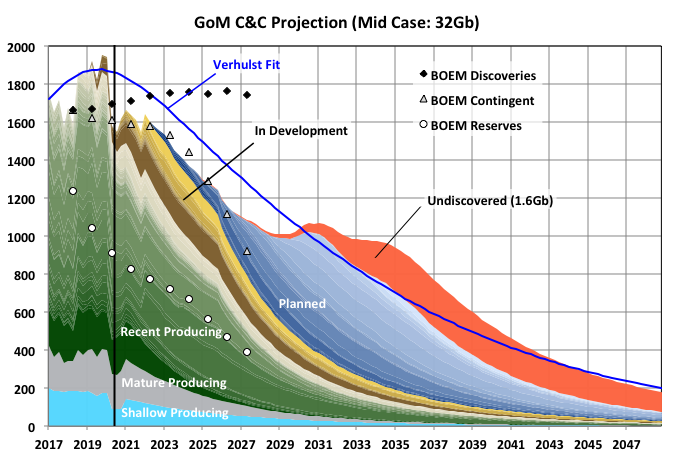

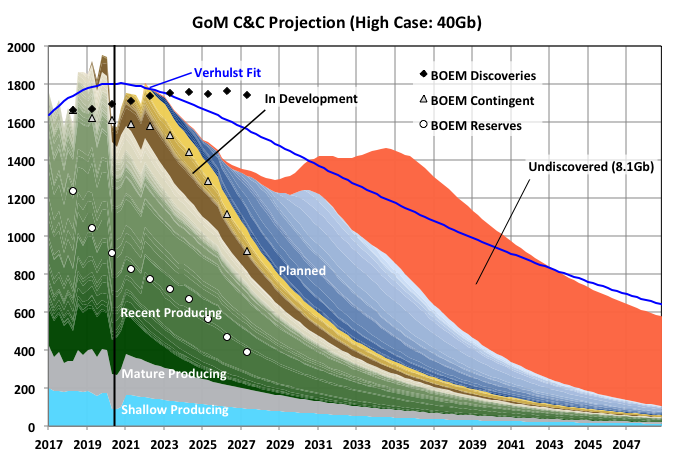

Future Production Scenarios

Below is an updated projected scenario (i.e. guess) for future production. The curves are adjusted so the total production in each section equals the estimated reserves for those fields from BOEM numbers for January 2016 less any production since then. Their estimates for this year (showing January 2017 numbers) have not yet been issued. For projects under development and discoveries I’ve used the E&P numbers for reserves, production and start-up where available or just made a guess. Numbers in brackets are nominal crude and condensate nameplate capacity for the expected development. I’ve included some nominal new discoveries with total reserves of 500 mmbbls, but may have to change that once the Whale numbers are announced.

I’ve also shown the 2018 BOEM production forecast, which I don’t fully understand. For instance they have on-line production suddenly dropping about 400 kbpd this year, but being made up with contingent numbers, which I would have assumed is possible development but can’t be; but also can’t be planned start-ups because there is nothing like that amount due this year. They also have a large amount of new discoveries that come on line very quickly – i.e. ten years to bring on line 800 kbpd, which would be some combination between eight big discoveries and eighty smaller tie backs. Nothing in recent history of exploration success or lease sales, or usual cycle times for deep-water projects, would suggest that is likely.

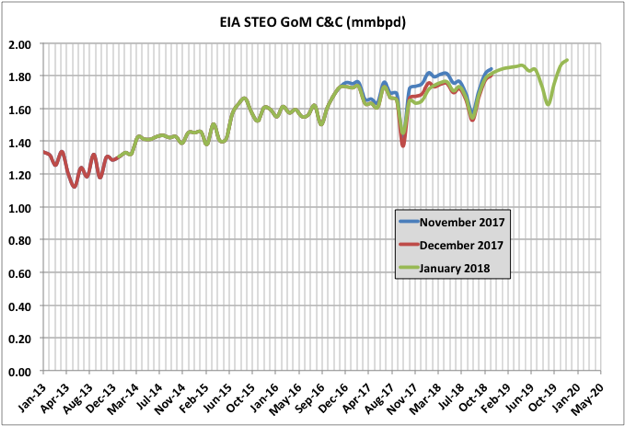

EIA STEO has its normal steady exponential rise, now extended through 2019, with bites out for hurricane season.

Off Topic Finish

Black domestic cats might be about to start to go extinct, as they don’t show up well on Instagram and the like. In one Bristol, UK rescue centre all forty cats that haven’t found homes are black. Owners of black cats are being particularly encouraged to get them neutered. The world is turning upside down.

2017 was the highest producing year for oil in the GoM and included the record month in March. Gas, which has tended to come from shallow water wells, had accelerated decline. The production would have been higher but for some disruptions from Hurricanes, in particular Nate, though that had the least impact onshore, and some unplanned outages in November and December due to equipment failures. The failure to Delta House subsea manifold affected Rigel, Otis and Son of Bluto 2 fields, and the first two still appear to be off-line while Son of Bluto 2 resumed production in December (LLOG, the operator, I think calls the Rigel field Neidermeyer, which is much better for the Animal House theme). The Enchilada gas pipeline appears to have ruptured at the main platform and has resulted in Baldpate, Salsa, Llano, Cardamom and Magnolia going off-line. Plans were recently announced to restart Baldpate/Salsa, which do not go through the platform, but I haven’t seen any notice of the restart.

Oil Average

Oil Exit Rate

Gas Average

Gas Exit Rate

Total Average

Total Exit Rate

(kbpd)

(kbpd)

(mmscfd)

(mmscfd)

(kboed)

(kboed)

2016

1600

1728

3308

3363

2151

2289

2017

1685

1570

2955

2381

2177

1967

Change

85

-158

-354

-982

26

-322

Ratio

5.3%

-9.1%

-10.7%

-29.2%

1.2%

-14.1%

C&C Production

December production numbers were dominated by the unplanned outages, so comparisons with November don’t mean much. As well as the two issues given above the Tahiti and Caesar/Tonga fields were off line for a few weeks, though I have seen no news why (these share a common set of leases but are produced separately to the Tahiti and Constitution platforms). Each month that these are three issues hold current outages would knock about 10 to 12 kbpd off the achievable average production for 2018.

Despite recent variability it certainly looks like the new fields brought on since late 2013, and which have seen all the net growth since then, have peaked. Any average decline rate can’t really be extrapolated yet, given the recent upsets, but the BOEM reserve estimate updates, due in the next couple of months, will provide better R/P numbers as there will be longer operating data for all the fields.

BP, Shell, Anadarko, Chevron and BHP have completed a lot of brownfield work and in-fill drilling to maintain production at their large, operated platforms, but they may be running out of options for the next couple of years, and there is some evidence of rising water cut in some of the larger leases at Shenzi, Atlantis and Thunder Horse (and also in West Boreas, a recent start-up for Shell in Mars-Ursa).

Natural Gas

Natural gas production saw accelerated decline through 2017, mostly from rapid decline of Hadrian South and the Enchilada outage. Shallow fields added some production late in the year, all from one lease in the Eugene Island area.

Apart from Hadrian South most of the gas from new fields is associated with the oil production and will decline in line with that. Otis is a small gas field that has been held offline by the Delta House outage.

The impact from the loss of Baldpate / Salsa production, which are mostly gas producers, is shown here, however also evident is how fast those fields had been declining anyway since 2014.

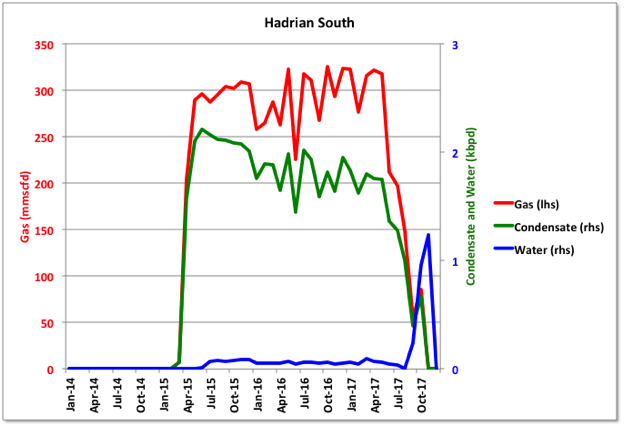

Hadrian South

Hadrian South looks to have finished. Production had been dropping fast since the summer and then, in October and November, water production appeared and gas flow stopped. On plateau it produced 300 mmscfd from only two wells, which is pretty prolific and slightly higher than planned. The wells had been producing about equally but one died between May and July and the second in November. Both were offline throughout December. Overall the field’s total recovery is lower than the BOEM reserve estimate, but only by about 38 bcf (6.5 mmbbls) so it’s questionable whether there will be any further efforts at increased recovery, certainly in the near future as there is no drilling rig contracted there, although there is another qualified lease for the field that has not yet been produced.

Production Wells Creaming Curves

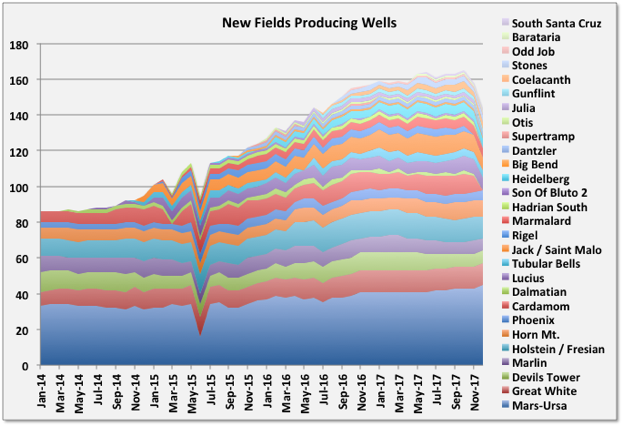

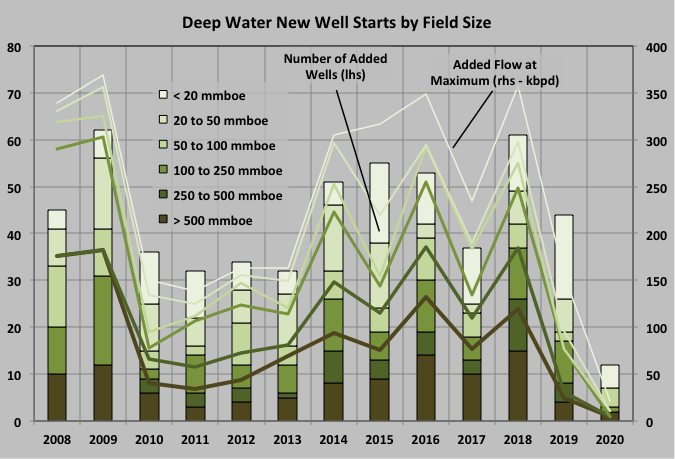

The following two charts show the number of producing wells for new fields and the larger, mature platforms. They both show how wells were added from 2014 through 2016, leading to the increased production in these two groups, but both numbers have now flattened off, which is likely to precede the start of a decline. For the new additions the move to tie-backs with one or two wells in 2016 and 2017 is evident and the continuous development at Mars-Ursa also stands out.

Drilling Activity

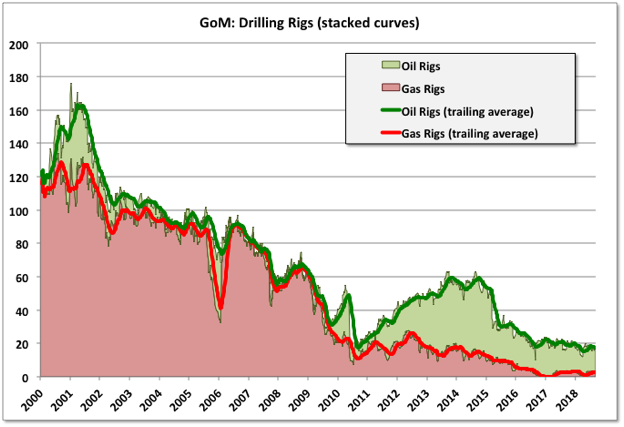

By Baker-Hughes active drill rigs averaged 20 in 2017 compared to almost 23 in 2016, and the numbers have continued to drop this year with a low of 13 earlier in March (the lowest since 2000, though the drop in shallow gas drilling is responsible for, by far, most of the change).

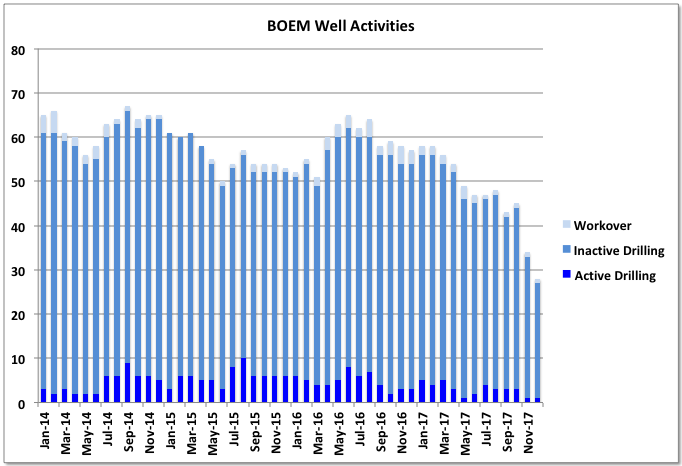

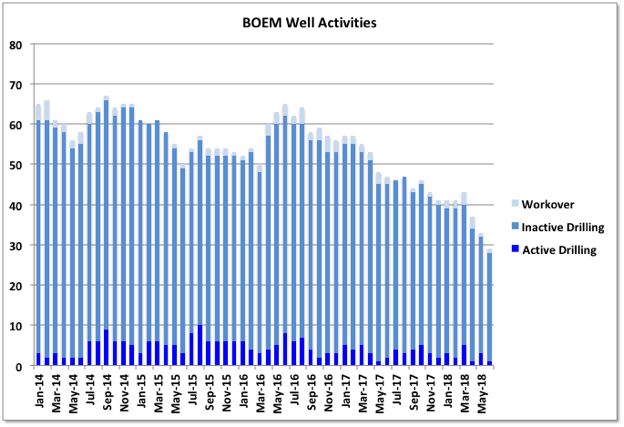

BOEM gives a monthly break down of each well by category, and it is noticeable how the number of wells being drilled has fallen off in the second half of 2017. (I think inactive wells are those that have not yet seen any production, but sometimes these are counted as “temporarily abandoned”, of which there are many and therefore it’s impossible to pick out new ones from old.)

2018 Plans

The Stampede platform started up in January. It has nameplate of 80 kbpd but some of that is for potential future tie-backs. The wells are pre-drilled and it should reach 50 or 60 kbpd streamday production quickly, though maybe not with high availability initially.

LLOG plan to bring several fields on line with one to three well tie-backs to existing platforms. However Red Zinger and La Femme / Blue Wing Olive go to Delta House. The subsea system is likely to be fixed when these are due, but the Platform was operating at nameplate capacity and with extended production deferral may not have processing capacity for these new wells this year.

Anadarko has planned five wells in existing fields, in particular for Constellation with BP, which will be about 15 kbpd. Anadarko have stated that they are looking at redeploying spar platforms onto other fields (probably for Shenandoah). I think that means one or more of their developments are nearing end of life, despite recent near field tie-backs, and that their remaining green field prospects are not very attractive at current oil prices. The platform mentioned was Marlin, though they have other mature Spar facilities like Holstein, which may impact LLOG as their tie-backs for Crown & Anchor are due to go there (but may have relatively short lives) and also is the site for two of this years new wells so maybe this is just conceptual speculation at the moment.

Big Foot is due at the end of the year. It was originally planned for 2015 start-up but had mechanical failures during installation, which are now fixed. Capacity is 75 kbpd nameplate. It is heavy oil and uses dry trees with ESPs. Two wells are pre-drilled but the rest only have the top two conductor sections ready, therefore ramp-up will be through 2019 as new wells get completed.

Off Topic Finish

This painting is by Mary Cassatt. There has been no better painter of children before or since. One theory for this is that she was a woman in, at the time, a man’s field, and the men all tended towards painting nudes; but maybe she was just really good at it. The greens in the carpet and blues in the chairs are gorgeous, though better in real life than here (it’s home is Washington DC), the dog is happier than it has any right to be, and I can’t help thinking the girl grew up to like an occasional night on the town.

BOEM has March 2018 production at 1696 kbpd, which is down 1% month-on-month and 4% year-on-year (March 2017 was the peak production month for GoM so far). EIA numbers were very similar, although last month’s were higher and haven’t been revised yet – typically EIA numbers end up almost exactly corresponding to the BOEM reported total qualified lease production, whereas BOEM can be a little higher, maybe including test wells or non-qualified leases.

The major new project, Stampede, started in January, has no reported production numbers yet. BOEM and EIA estimate non-reported values and then retrospectively adjust their reports when actual numbers are available. I don’t know how they estimate new production but Stampede could produce around 60 kbpd with current plans, though likely a lot less initially as only one of two leases has been ramping up. I’ve assumed 20 and 40 kbpd for February and March respectively, which still might be high. Even allowing for that, and assuming other late numbers are the same as the previous month, since December EIA and BOEM both have estimates about 30 to 40 kbpd higher than the reported lease and well production numbers (which always match closely) would suggest. Usually the difference is no more than ten. It is unlikely that the other late numbers, of which there are few, and none for all four months, will show such large, sudden and unexplained increases so either I’m missing something (maybe a lease not yet included in the numbers, but also not reported as starting up) or there could be some future downward adjustments.

Rigel and Otis are still off-line following the failure at a subsea manifold last October and are taking out about 22 kbpd plus some gas (Otis is a small gas field). Great White, Stones (for the full month) and Caesar/Tonga all had noticeable downtime in March taking about 90 kbpd off-stream.

The Kaikias Phase I development for Shell, a tie-back to the Ursa hub, was brought on line one year ahead of schedule in early June. It has an expected peak nameplate of 40 kboed (which may only be around 30 kpbd average oil), and will likely take a bit of time to ramp up to maximum. Equally to accelerate production like this probably meant using a drill rig that was previously scheduled for alternative wells on Mars-Ursa, so there may be faster than previously planned decline on some of the other leases there.

In the second quarter there is likely to be downtime showing for Marlin, Horn Mountain and Holstein as they have planned turnarounds to prepare them for new production and, presumably, to allow normal maintenance; they should then come back online with higher overall flows. Marlin has one new Anadarko well planned, plus two from LLOGs Crown and Anchor field. Holstein has a platform rig and is developing four side-track wells this year and next. Horn Mountain has one more tie-back from Dorado field planned.

Atlantis has no drilling or work-over activity currently shown and in the past its wells have declined at around 20% year-on-year (see below), which may continue until the first Phase III wells come on line in 2020.

Llano, Cardamom and some of Baldpate/Salsa production came back on line following the partial repair of the Enchilada pipeline, adding around 45 kbpd, but there is some still off line, which I think has to be processed through the Enchilada platform and for which I’ve seen no expected restart news; however Anadarko have said it will be “later this year”, which I’d take to mean a few months yet. All these fields are fast declining so although they give a jump for March they will result in steeper declines for the remainder of the year

The BSEE deep-water activity report showing wells with drilling, completion, P&A or work-over activity currently shows 40 actions, this is down from around 50 at the beginning of the year and has been fairly steady for the past two months.

Overall C&C looks to be continuing an overall slow decline started in the second half of last year, and if the unaccounted for 40 odd kbpd is revised out, then it is clearly accelerating. A lot will depend on downtime for turnarounds and hurricanes. So far this year these losses look higher than last (e.g. the early Tropical Storm Alberto took out about 7 kbpd for about a week, and also disrupted P&A activity on Lena and installation work at Appomattox) plus Mars-Ursa looks set for a partial shut down in April and the current Perdido / Great White turn around looks to be quite prolonged. Another major unplanned outage, like Enchilada or Delta House, is also possible. The Kaikias development by Shell has been advanced, but that may be countered by delays to Constellation, Hadrian North and some Delta House tie-backs.

Natural Gas

Natural gas production is in continuous decline. BOEM had March production at 2.59 bcfd, down 1% month-on-month but 21% year-on-year. The loss of 300 mmcfd from Hadrian South since last year and the losses from Baldpate / Salsa, one of the few other remaining significant gas fields, and Otis, because of the Delta House failure, meant last year showed accelerating decline which is unlikely to recover. Na Kika has a few gas leases, and a new long distance tie-back, Coulomb II, is due soon, but mostly the gas now is associated with the oil and will decline accordingly.

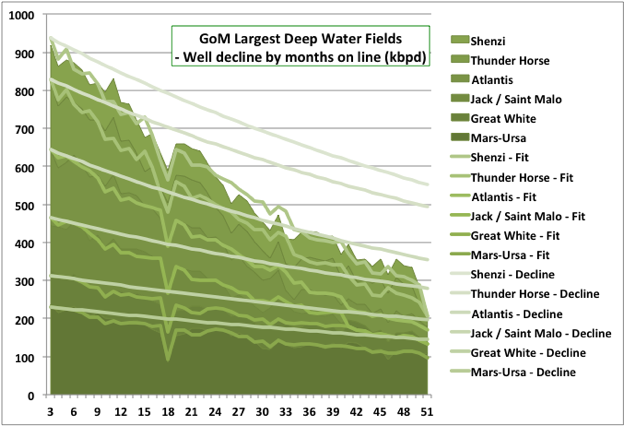

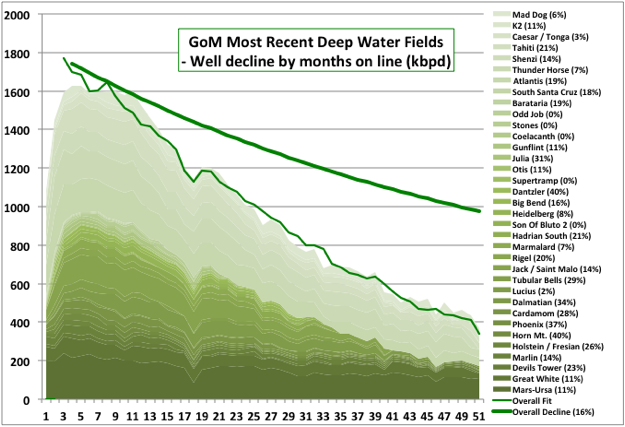

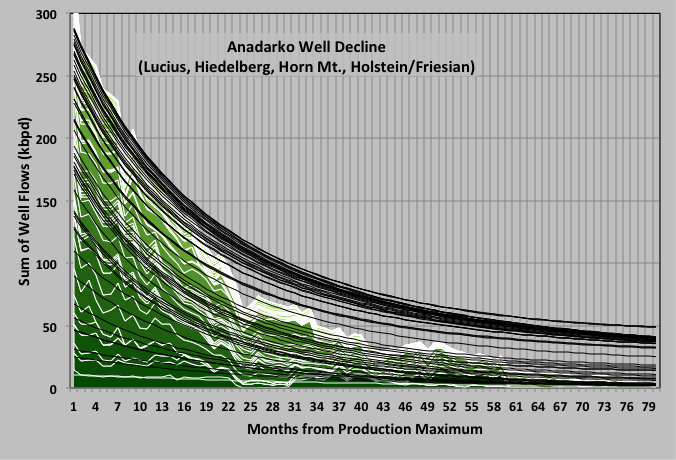

Deep Water Well Decline Rates

I had a go at finding the decline rates of the wells in the more recent deep-water fields. In the charts below for each field all the wells are lined up so month one is their first production or January 2014, whichever is later, and a decline curve is fitted, from the third operating month to avoid the ramp-up period, assuming all wells in a field follow the same exponential decline and according to how many wells were producing for each month.

Most of the fits came out reasonably well. Six of the largest fields are shown in detail below. The overall (stacked) decline curves indicate the expected decline rate for all the wells remaining online, they are not predictions of future production.

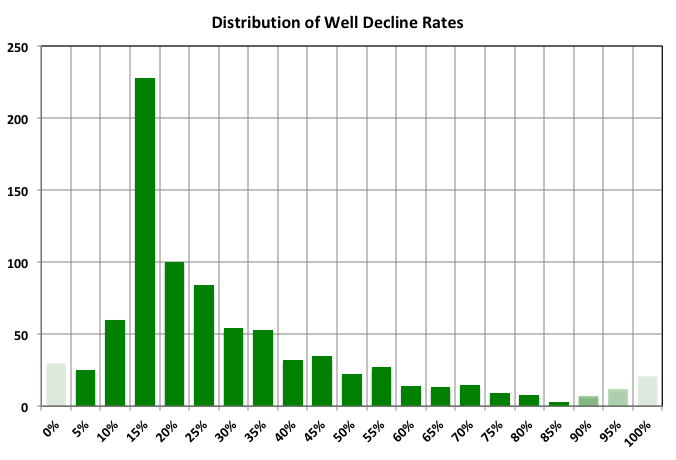

The fields where the fit was poor were either new projects that are still on plateau, have had fairly patchy start-ups, or have produced a lot of water (or all three) and include Lucius, Stones and Odd Job; or ones where there has been some sort of well rework, e.g. K2, which had gas lift added, and Mad Dog, which had various new measures including water injection added on some blocks. I didn’t include Na Kika as it is a collection of several different fields, some of them gas, and has a pretty uneven production history. The individual decline rates for each field are shown in parentheses after the name and run from 0% for fields on early plateau, up to 40% and with a pretty good spread between.

The decline rate for the fields analysed is likely to increase because of new projects coming off plateau, water breakthrough or acceleration (e.g. at Great White, Mad Dog, Lucius and Mars-Ursa might be the most likely) and a normal development feature that the best wells are drilled first; but overall that would likely be balanced by new projects reaching plateau. The overall average decline rate came out as 16%, which is maybe not surprising given that depletion rate for the whole GoM based on BOEM 2P numbers for 2016 (the latest available data) was also 16%. With depletion and decline close it would imply there isn’t much being added to reserves on operating fields, or any that has been was quickly put on-line.

Applying these decline rates to the 2017 field production rates gives an expected drop this year of 175 kbpd. Shallow fields are likely to decline 30 kbpd and the deep-water fields that I didn’t include about 45 kbpd. So total would be 250 kbpd; assuming 90% availability that would require 275 kbpd of additional nameplate capacity added to hold production steady.

2018 and 2019 Developments

The only certain major new fields this year are Stampede, adding up to 60 kbpd, and Kaikias Phase I, which may add about 20 kbpd averaged over the year. Constellation was due but looks to have been pushed into 2019, and Big Foot is due late but may not contribute much to the average, although could boost the 2018 exit rate. There are four smaller field tie-backs for LLOG with one or two wells: Red Zinger, Crown and Anchor, Claibourne and La Femme / Blue Wing Olive. Some of these may be limited by available capacity at the host, and will contribute only in the second half of the year. Recent small field wells tend to start at around 6000 to 8000 bpd and immediately decline, but those fields together could add 50 to 60 kbpd at end of year. Bigger wells are likely to come from in-fill and development drilling at Jack / St. Malo (two wells), Horn Mountain Deep and Marlin for Anadarko (three wells, but very high decline rates if they are like the recent ones), Tonga (I think one last production well), one side track well at Holstein (with three more next year), continued BP drilling at Thunder Horse, and Shell projects at Mars-Ursa, Stones and Great White. BP and Shell wells may add the most but they are also the ones with the least information.

There should be some offline production returning at Rigel and Baldpate, maybe 40 kbpd, but also fast declining. With the new fields that would leave 120 to 180 kbpd needed this year from the in-fill drilling to keep annual rates about average (the range is dependent on the timing of all the wells coming on); I think that is going to be difficult. Next year decline is likely to accelerate because a lot of the mentioned in-fill wells and tie-backs are the last available for those projects and some of the rigs are being released, plus Kaikias has been accelerated, so will contribute less additions next year than originally planned. Atlantis Phase III has also been moved back to 2020. 2019 has some planned continued development for Thunder Horse, tie-backs for Hadrian North and Buckskin to Lucius and the delayed Constellation tie-back to Constitution, but overall things look thinner than this year, at least until Appomattox (with 175 kboed nameplate) begins ramp-up towards the end of the year.

The drop off in the number of wells showing drilling or work over in the chart below highlights the possible slowdown coming in 2019.

Better projections will be possible when the BOEM reserve estimates for the end of 2016 are available. These are quite late compared to last year, but in the past they have come out in July or August, and EIA reserve estimates were also pretty late this year.

Among the fields given it lists significant new oil production as expected from: Amethyst, a small and failed gas project and Phobos, both of which are rescinded leases with no current activity; Otis, an existing gas field; Son of Bluto 2, a small oil field started in early 2016 with no current drilling and indicating slight decline; Rydberg, a recent Shell discovery with reported 100 mmboe resource base, which I think would be a later addition to the Appomattox project; Gotcha, a lease which is part of Great White, started in 2014 and in slow decline; and Bushwood, a single gas well tie-back started in 2014 and now almost exhausted (although there has been some drilling there this year). There is little new oil, or much significant oil at all, in that collection.

It does also list Horn Mountain Deep, Stampede (though listed as two fields, when it is really only one) and Kaikias, which will be bigger contributors, but not enough by far to meet the given growth expectations (and I think the Horn Mountain developments will be showing rapid decline by next year).

It does not mention Big Foot, Appomattox, Buckskin, Hadrian North, Red Zinger, Crown and Anchor, Claibourne or Blue Wing Olive as new fields, or the Thunder Horse developments and other Anadarko in-fill wells. I don’t know how they come up with their assessments but they seem to be getting more removed from actuality, and not just from being overly optimistic. Similarly the EIA STEO is just a constant exponential growth that is re-zeroed each month to current production figures with no changes made based on FID decisions, reserve numbers or overall production history.

Off Topic Finish

As the last country music link went down fairly well here is another. Two minute thirteen seconds of downbeat alt.country bliss. It’s the title track of an album that I always expect to see in ‘Top XXX’ lists, but never have, which shows how much I know. The singer and writer, Willy Vlautin, also writes books, one of which, “Lean on Pete,” was made into one of my favourite films of the last year, a classic American road movie with a sort of happy ending (though not for Pete). Richmond Fontaine

And here is Vlautin’s new band, more traditionally country, with an apposite song (I think the singer is the sister of the vocalist on the previous tune). The Delines

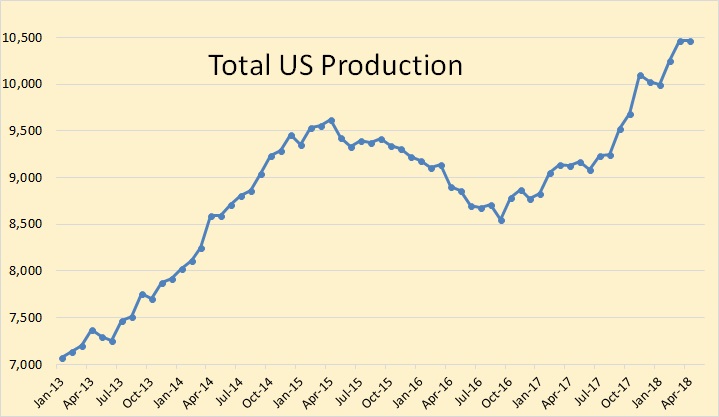

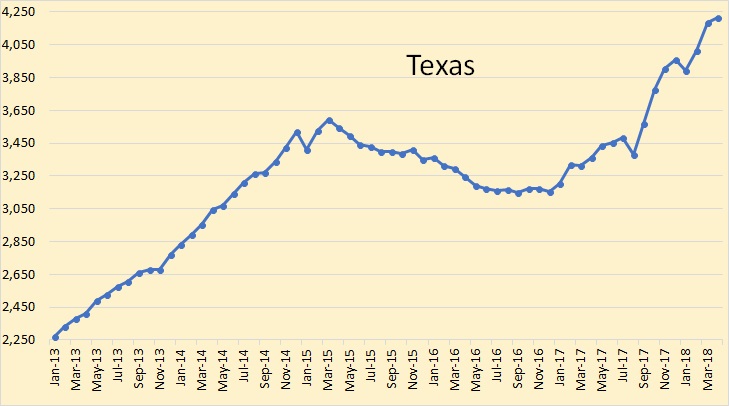

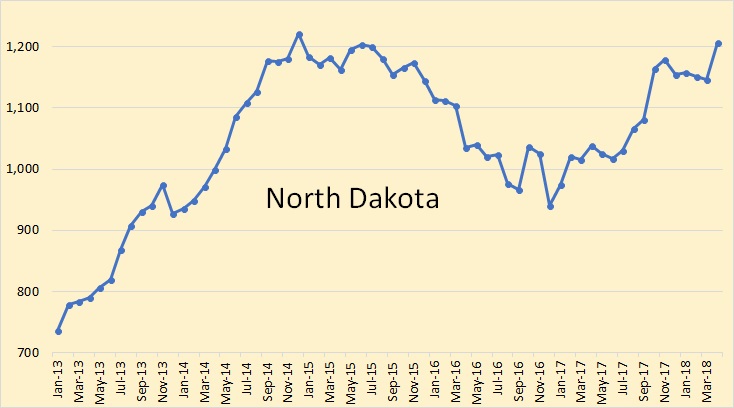

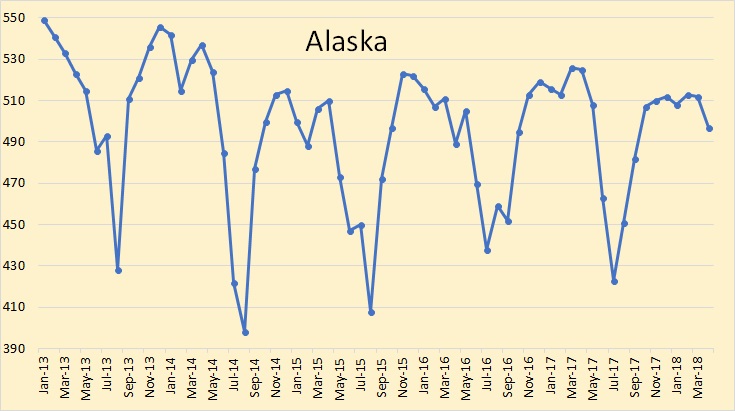

All data below is from various sources. All US data is from the EIA. Unless otherwise noted is in thousand barrels per day.

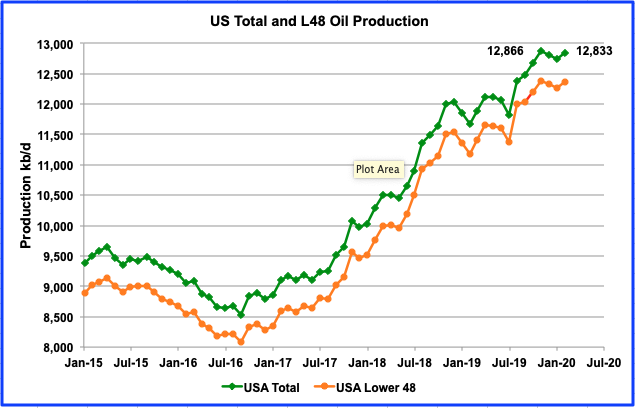

USA data is through April. C+C production was almost flat in April, down 2,000 bpd.

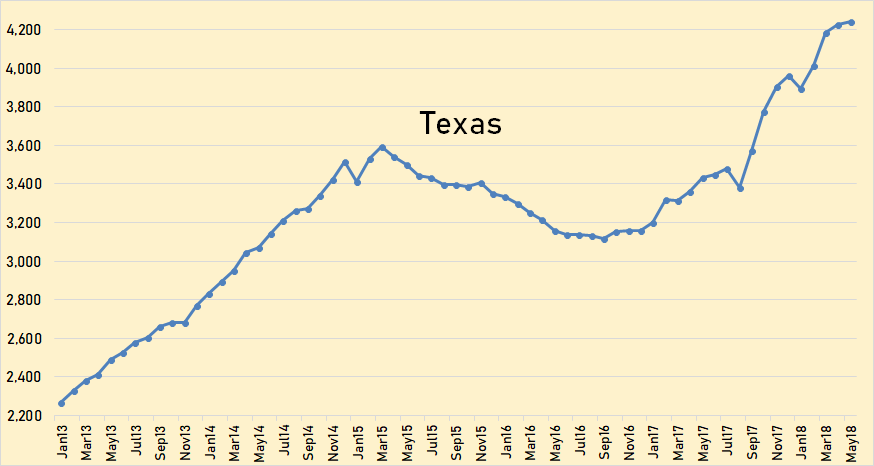

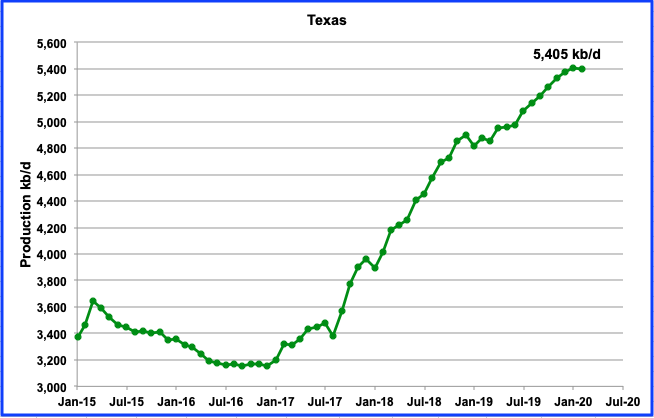

Texas through April. Texas production was up 30,000 bpd in April.

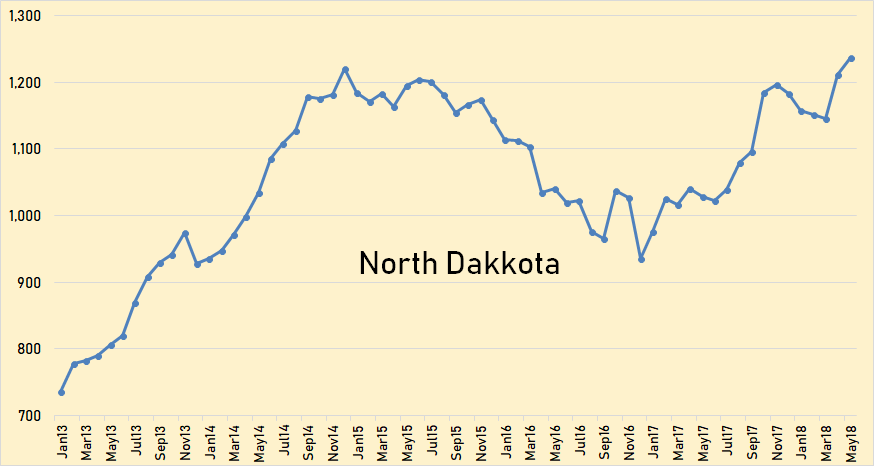

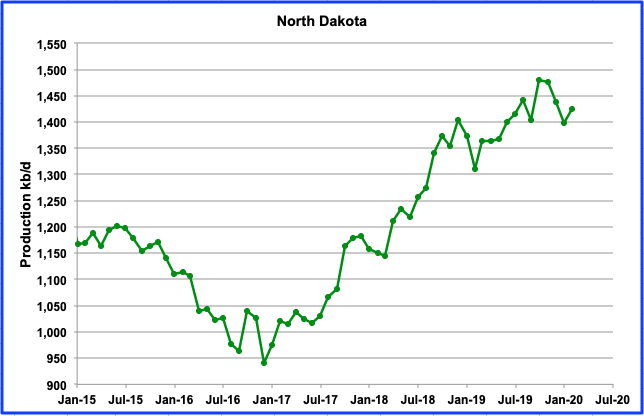

North Dakota through April. North Dakota production was up 61,000 bpd in April.

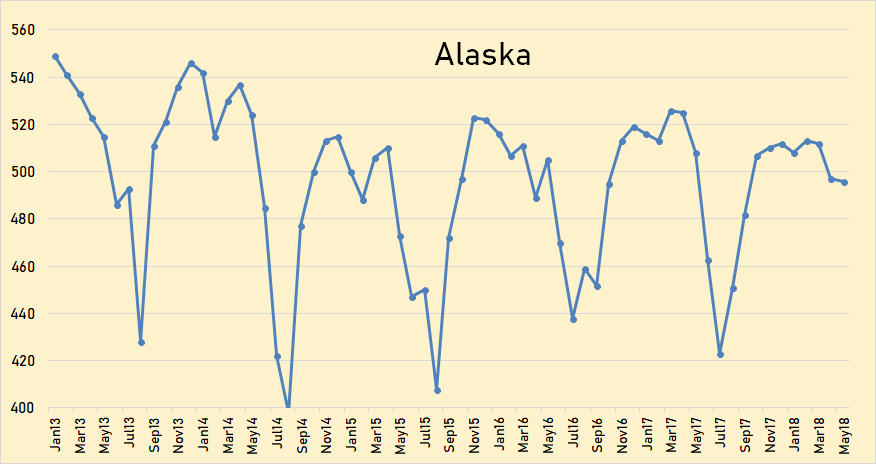

Alaska through April. Alaska production was down 15,000 bpd in April.

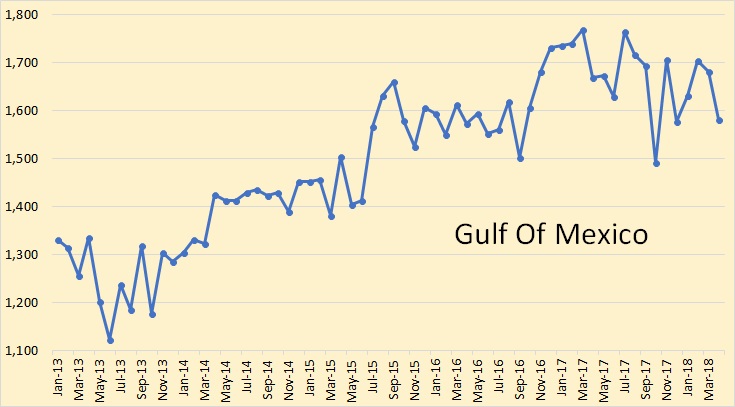

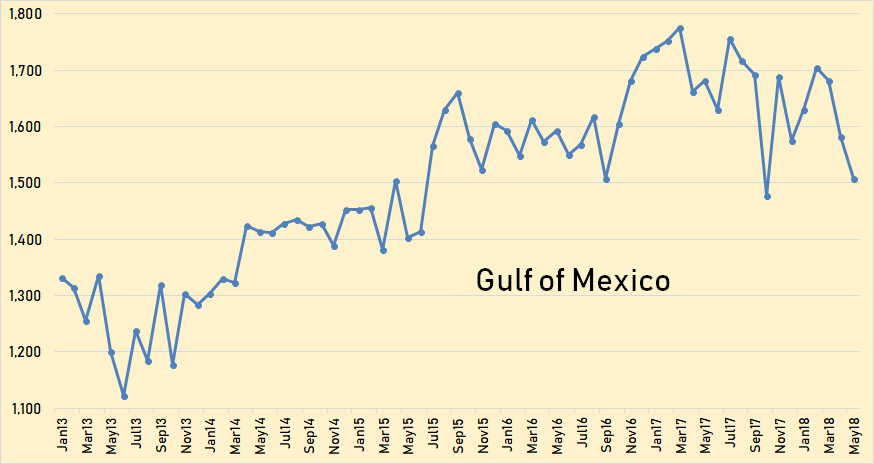

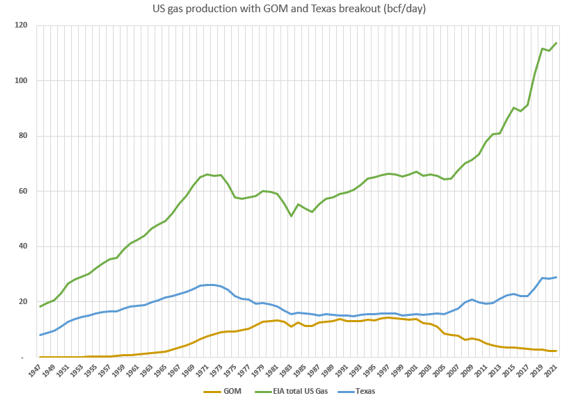

The Gulf of Mexico through April. The GOM was down 98,000 bpd in April.

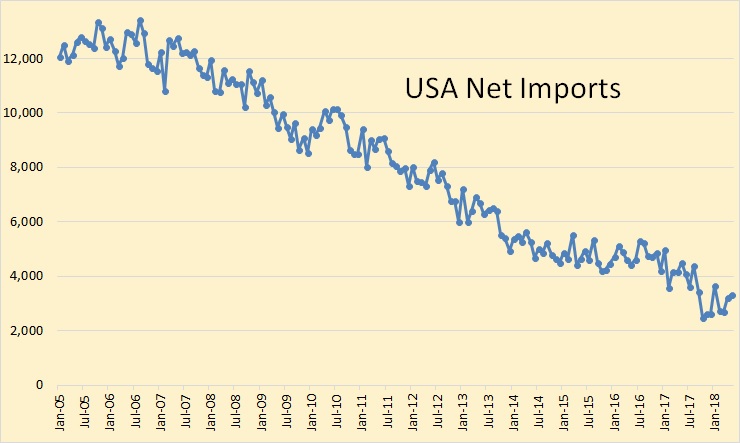

USA net imports averaged over 12,500 kbpd in 2005 and 2006. They are now down to around 3,400 kbpd.

China data through March from the EIA.

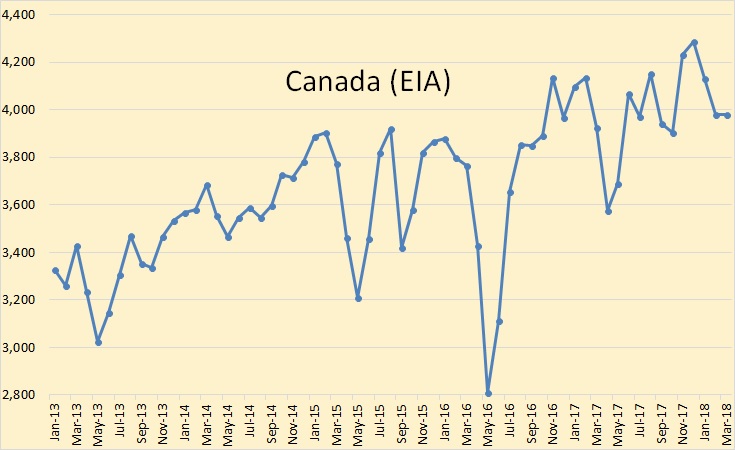

Canada through March, EIA.

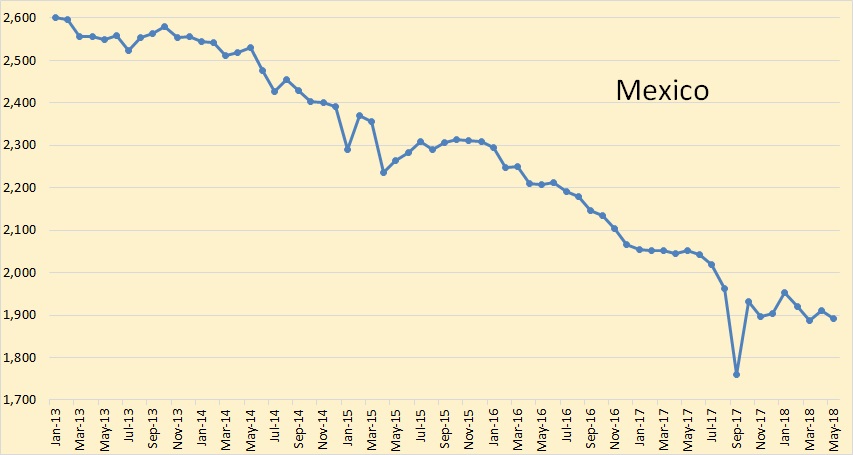

Mexico through March, EIA.

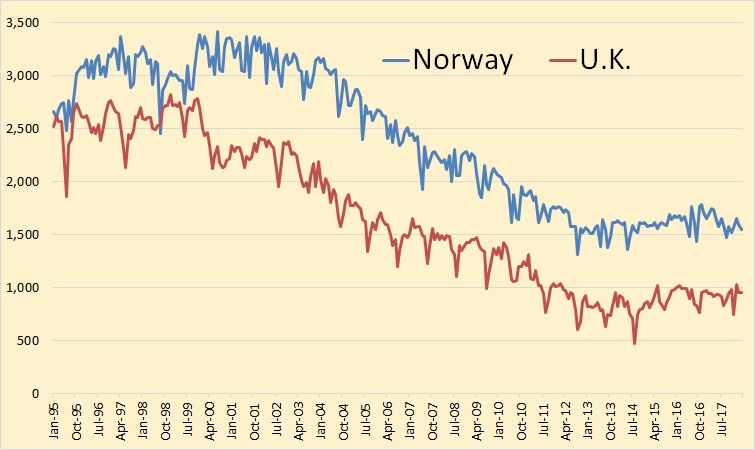

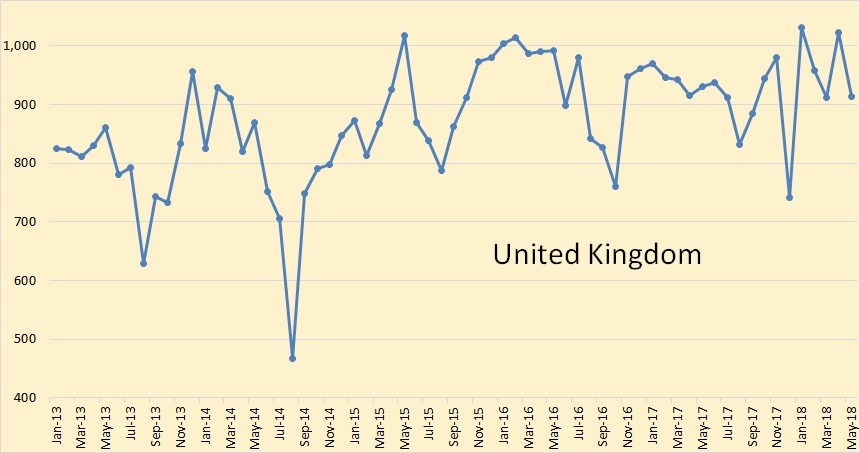

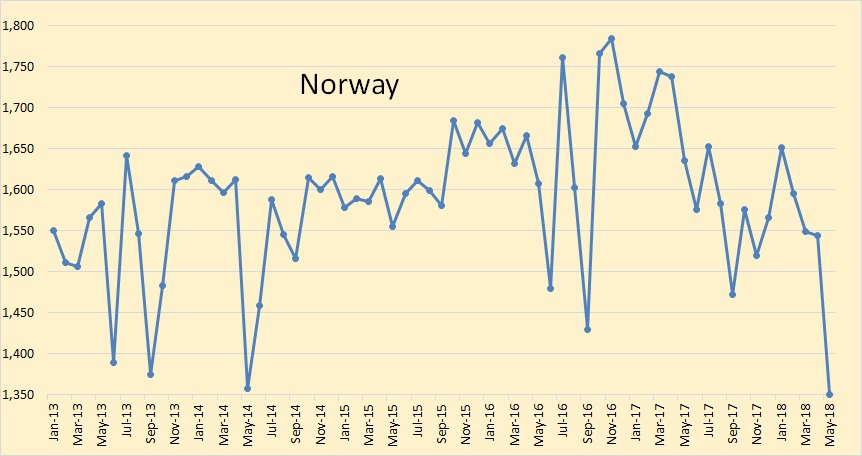

Norway and the U.K. through March. I have included historical data here in order to show the total decline from their peaks around the turn of the century. There has been a recent uptick in production from both countries.

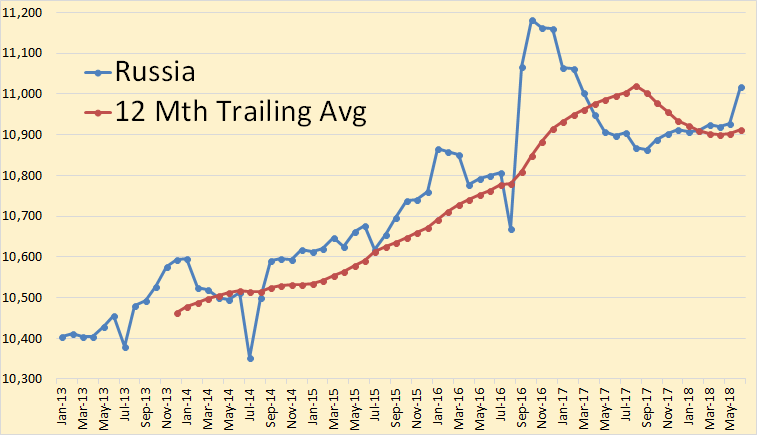

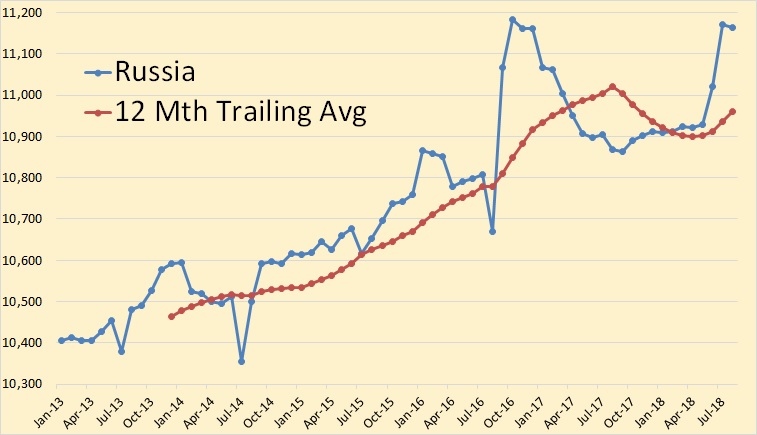

Data for this chart is from the Russian Minister of Energy and is through June. Russian production was up 89,000 bpd in June.

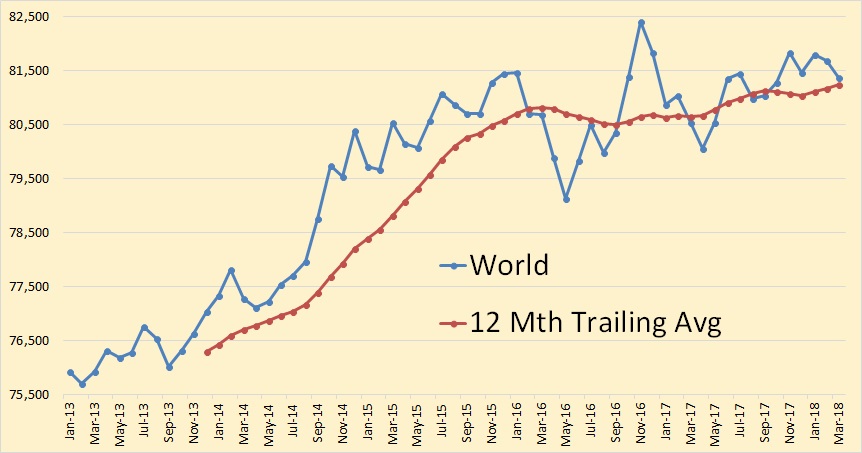

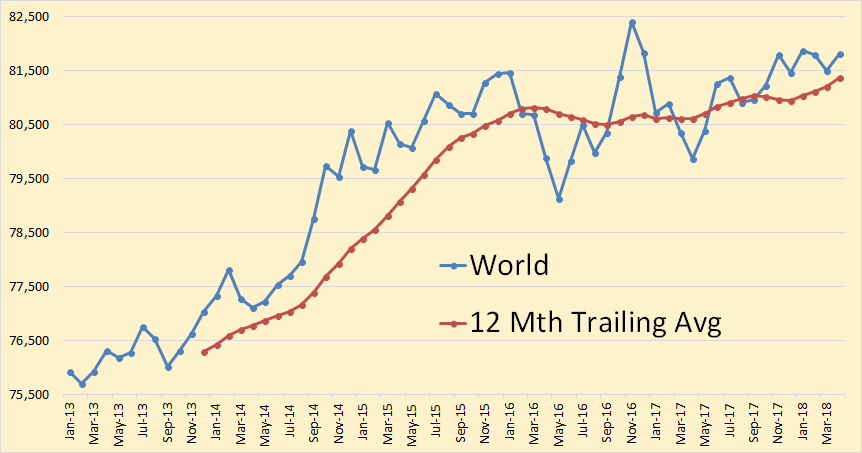

World production through March. World C+C production was down 305,000 bpd in March.

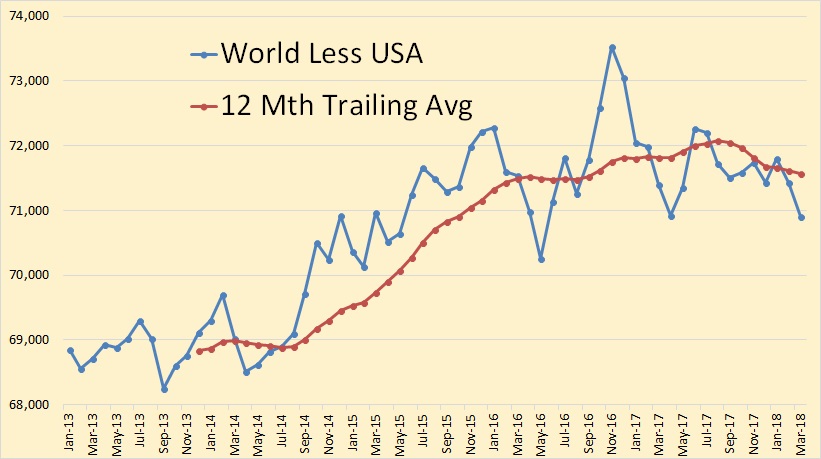

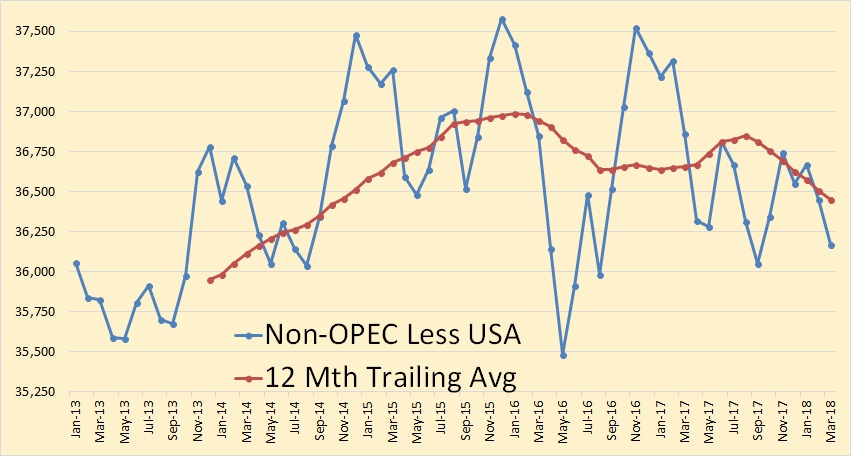

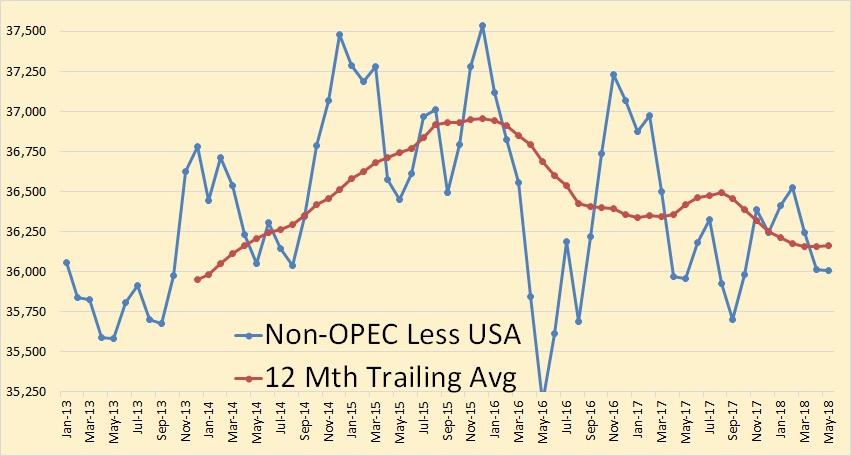

World less USA through March. Without the US input, World C+C would have been down 520,000 bpd in March if the EIA’s figures are correct.

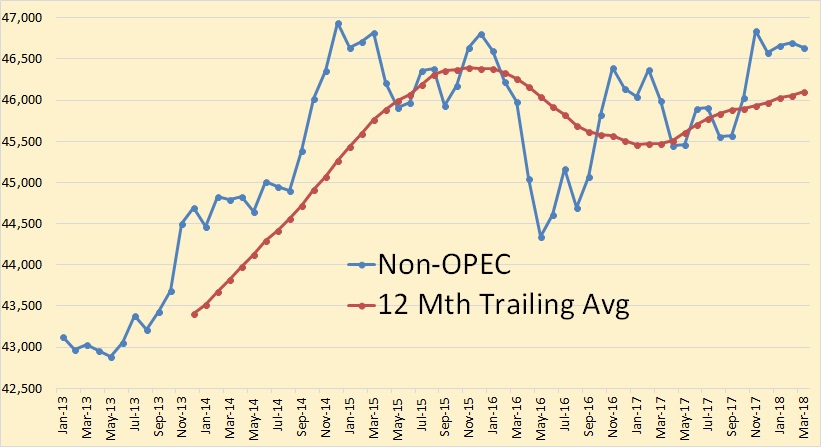

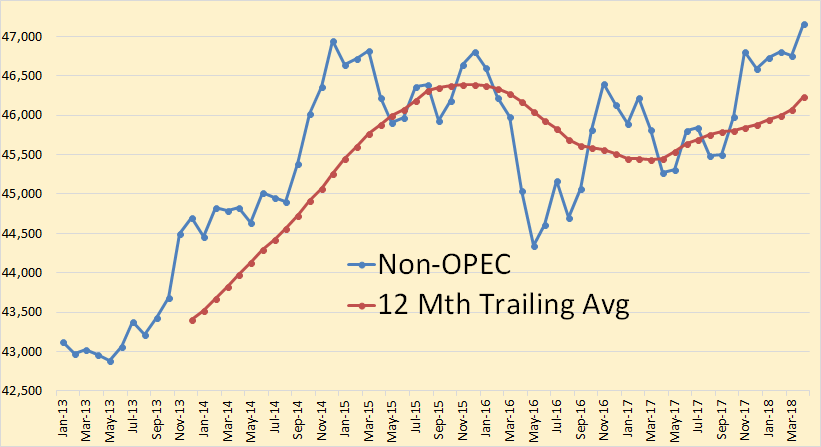

Non-OPEC production was down 63,000 bpd in March.

Without US production Non-OPEC would have been down 278,000 bpd in March.

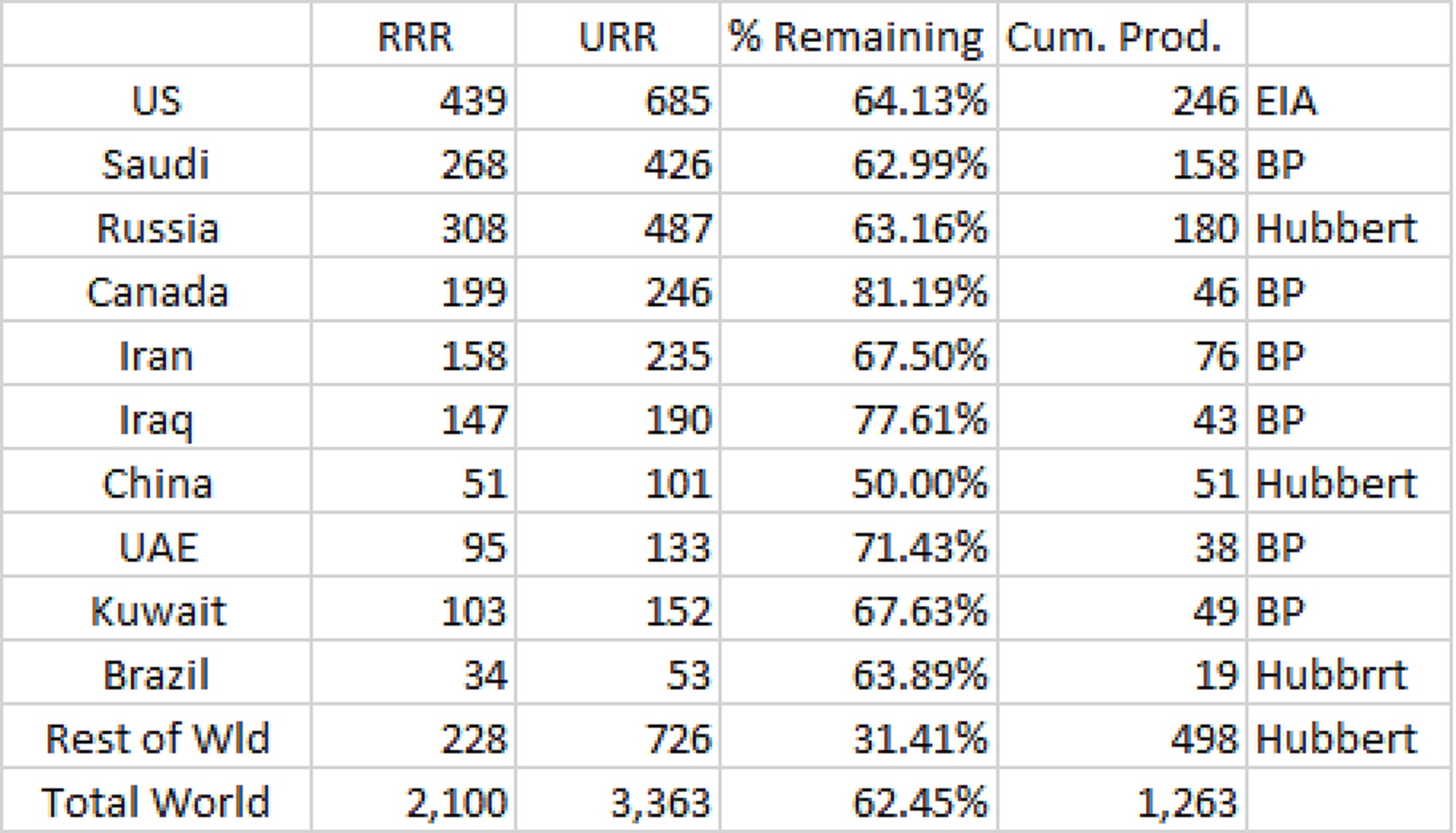

I don’t do natural gas or coal but I do have a few comments on his oil numbers. In the table below I have converted metric tons to barrels using 7.33 barrels per ton. All data is in billion barrels. I have calculated cumulative production by subtracting RRR from URR. Even though their estimate of URR may be highly inflated, and I believe it is, this makes no difference because they calculated RRR by simply subtracting cumulative production from their estimate of URR. I simply reversed that process.

All data is crude plus natural gas liquids. Of course, that includes condensate.

I think the EIA data for the US is highly inflated. They are grossly overestimating the input from shale oil here. The BP data for OPEC, obviously what BP has done here is just to take each OPEC nation’s word for their reserves. I have no comment on their Canadian numbers.

The Hubbert Linearity method was fairly accurate before the age of creaming. As long as conventional wells were used, the Hubbert method gave you a pretty good estimate of URR. And you could also calculate the probable decline rate with the Hubbert method. But no more. A field is creamed by massive infill drilling with horizontal wells that skim the very top of the reservoir. The decline rate is then drastically reduced while the depletion rate is drastically increased. Things will go just great until the water hits those horizontal wells at the top of the reservoir. Then production will drop like a rock.

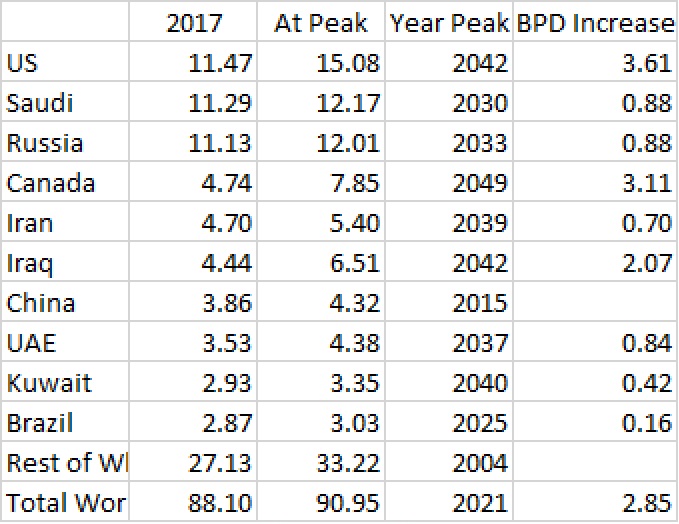

The field has produced more than 15 billion barrels since operations began in 1960. Last year’s annual production was around 290 million barrels, though that should fall to around 234 million barrels by 2020, the employee at PetroChina said in an interview published Sunday.

In 2015 Daqing produced about 800,000 barrels per day. If it were to produce 234 million barrels in 2020 then that would be about 640,000 barrels per day or a decline of about 160,000 bpd. Looking at the chart below I think those figures are extremely optimistic.

China’s production has dropped by over 400,000 barrels per day in the last three years. And the lions share of that decline has to be Daqing.

In the table below I have converted the data Dr. Minqi Li presented in metric tons per year to million barrels per day. Again, this is C+C plus natural gas liquids.

The source for this chart is the same as the table above. I believe due to OPEC massively inflating their URR, and the inaccuracy of the Hubbert method due to the creaming of all giant fields, the expected peak dates here are highly inaccurate. Well, all except three. The rest of the world did peak in 2004, China did peak in 2015, and the world will peak by 2021 or before. Congratulations to Dr. Minqi Li, the most accurate future peak there is the one that he calculated.

Here are the latest oil production numbers from the EIA. All data is in thousand barrels per day unless otherwise noted.

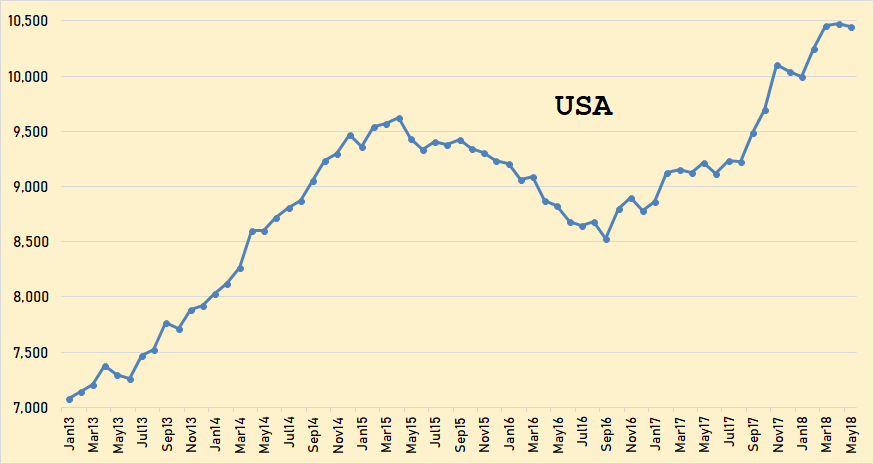

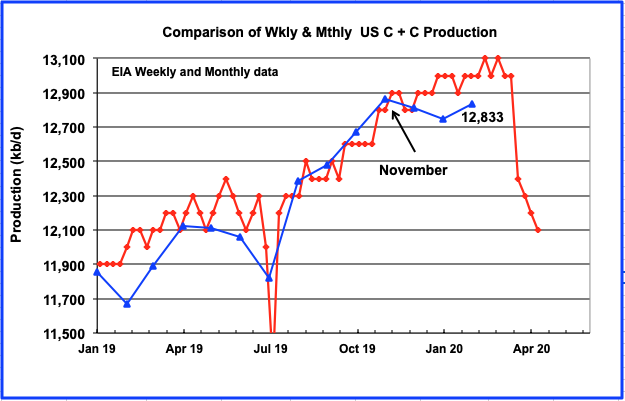

The USA through May 2018. The upward surge has stalled for the last two months. US production was down 30,000 bpd in May.

It is a little astonishing how close the Texas chart resembles the USA chart. Texas is, by far, the USA’s largest producer. As Texas goes, so goes the USA. Texas production was up 20,000 bpd in May.

North Dakota production has increased significantly in the last two months. They were up 67,000 bpd in April and up another 25,000 bpd in May.

Gulf of Mexico production was down 99,000 bpd in April and down another 75,000 bpd in May.

Alaska was down only 1,000 bpd in may but that was 12,000 bpd lower than last may. They are now entering the maintenance season. Expect huge drops in June and July.

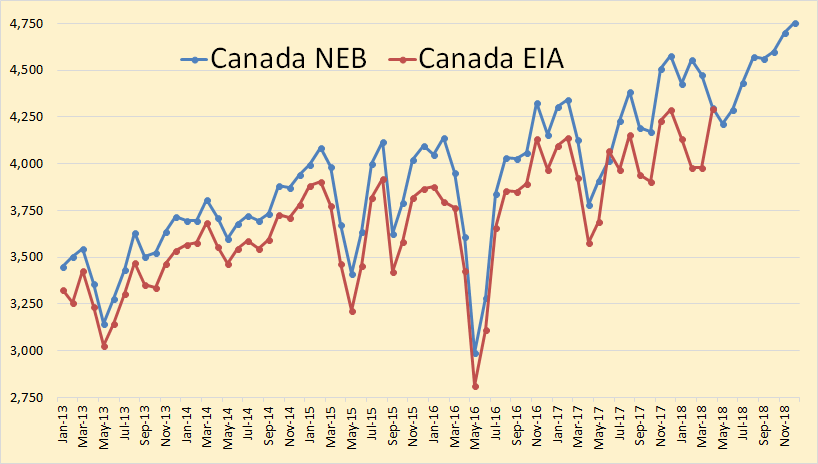

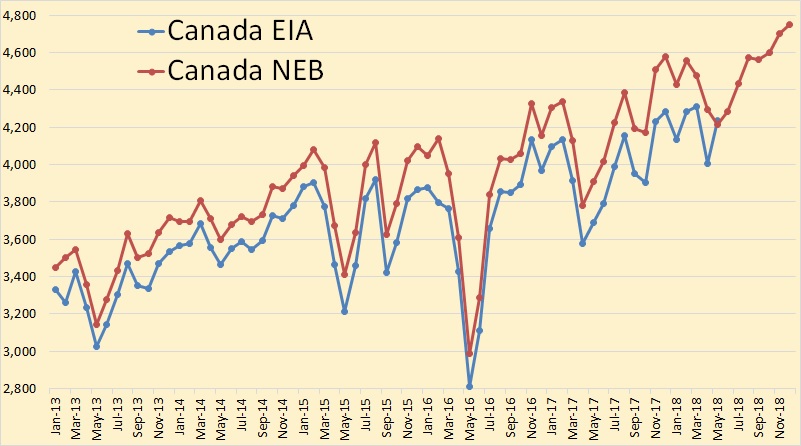

The EIA data in this chart is through April and the National Energy Board data is <b>estimated</b> through December 2018. The EIA data is usually lower than the NEB data but they both agree on April production.

World crude oil production was up 326,000 bpd in <b>April.</b>

Non-OPEC production reached a new peak in April, up 405,000 bpd to 47,159,000 bpd. Most of that increase was Canada, up 317,000 and the U.K., up 111,000 bpd.

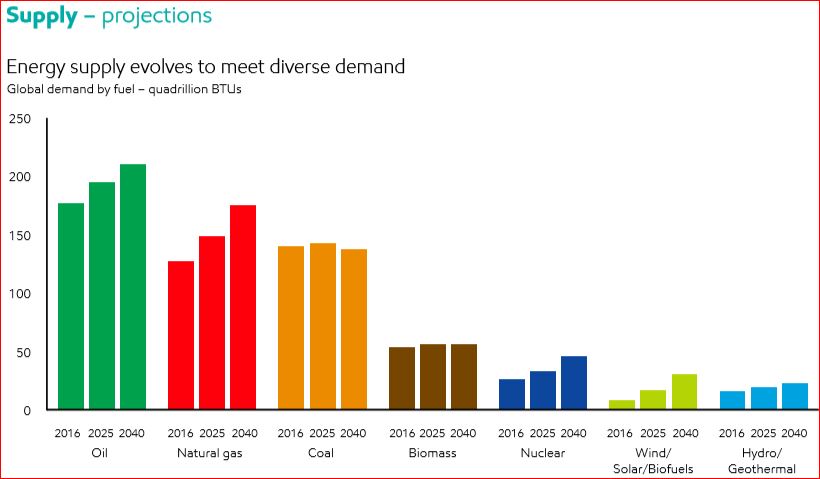

Here I am adding a few charts and comments from ExxonMobil’s 2018 Outlook for Energy: A View to 2040. Their text is in italics. Any bold in their text is mine.

• Technology improvements lead to wind, solar and biofuels increasing, with a combined growth of about 5 percent per year • Non-fossil fuels reach about 22 percent of total energy mix by 2040 • Oil continues to provide the largest share of the energy mix; essential for transportation and chemicals • Natural gas demand rises the most, largely to help meet increasing needs for electricity and support increasing industrial demand • Oil and natural gas continue to supply about 55 percent of the world’s energy needs through 2040 • Coal’s share falls as OECD countries and China turn to lower-emission fuels • Nuclear demand grows 70 percent between 2016 and 2040, led by China • Wind, solar and biofuels reach about 5 percent of global energy demand

They assume that supply will always evolve to meet demand.

This is what they say we will need in 2040 and will therefore be delivered by technology.

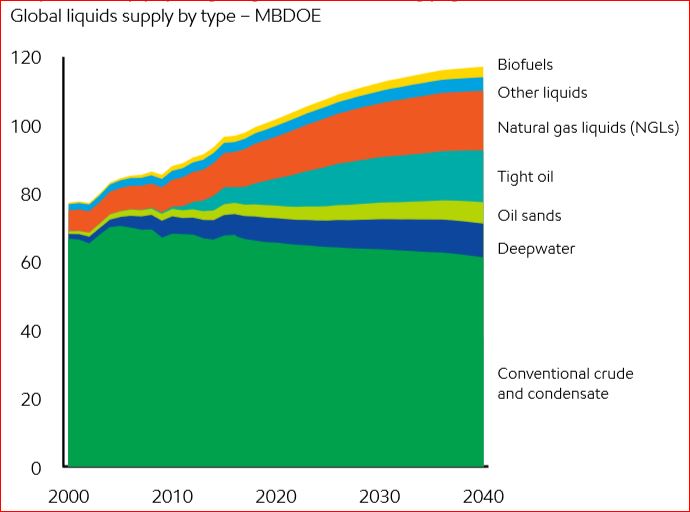

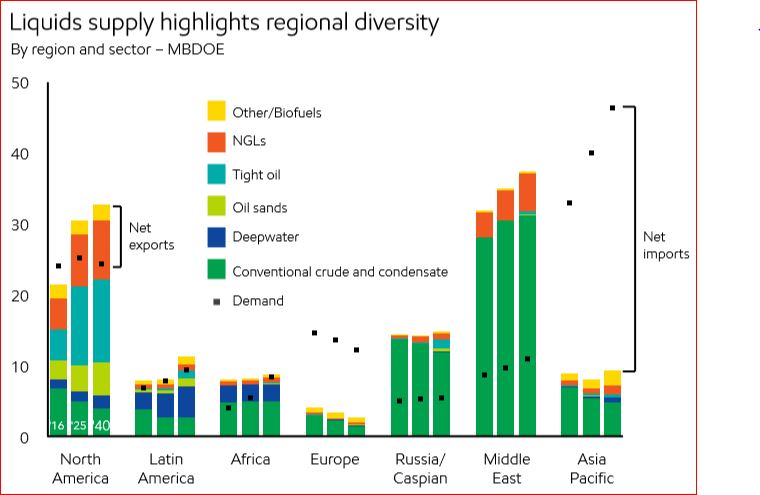

And here is where all that oil will come from. North America is the US and Canada. They count Mexico as part of Latin America. In 2040 they have total North American conventional production down to about 3.5 million barrels per day. They have at about 12 million bpd and oil sands at about 4.5 million bpd as best as I can eyeball the chart.

They have almost all conventional oil coming from the Middle East and Russia/Caspian. Caspian is mostly Azerbaijan.

• Global liquids production rises by 20 percent to meet demand growth • Technology innovations lead to growth in natural gas liquids, tight oil, deepwater, oil sands and biofuels • Technology enables efficient production from conventional sources, which still account for more than 50 percent of production in 2040 • Most growth over the Outlook period is seen in tight oil and natural gas liquids, which reach nearly 30 percent of global liquids supply by 2040 • Continued investment is needed to mitigate decline and meet growing demand • Liquids trade balances shift as supply and demand evolve • North America swings to a net exporter as shale growth continues • Latin America exports increase from deepwater, oil sands and tight oil supplies • The Middle East and Russia/Caspian remain major oil exporters to 2040, and Africa shifts to an importer • Europe remains a net oil importer, as demand and production both decline • Asia Pacific imports increase to 80 percent of oil demand in 2040

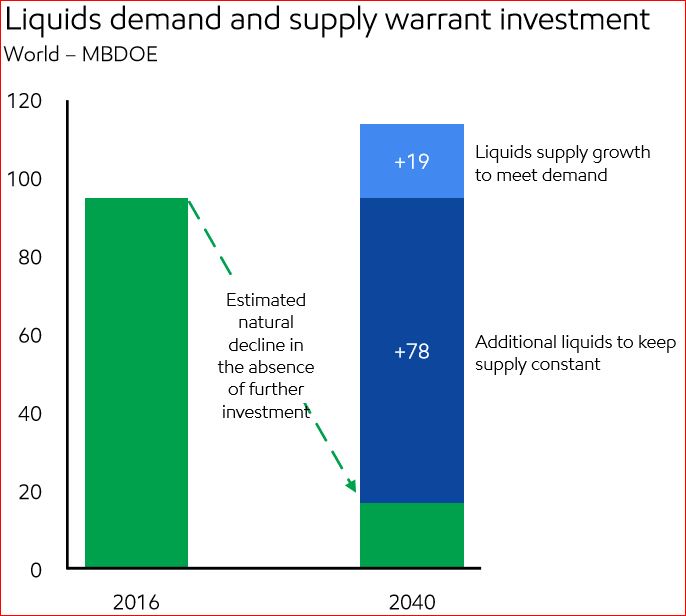

This chart is a little shocking. They have total liquids declining to about 18 million bpd by 2040 without investment. That means if everyone stopped drilling today, or in 2016, that would be the natural decline of what is online today. But to meet demand we will need 97 million barrels per day of new oil.

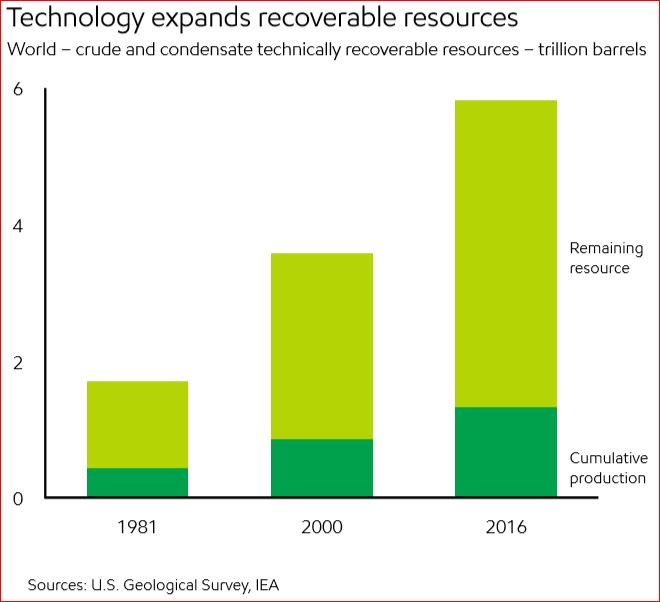

And this is what they say we have left, about 4.5 trillion barrels of remaining recoverable resources.

• Without further investment, liquids supply would decline steeply • More than 80 percent of new liquids supply needed to offset natural decline • Per the International Energy Agency, about $400 billion a year of upstream oil investment is needed from 2017 to 2040 • Global oil resources are abundant • Oil resource estimates keep rising as technology improves • Technology has added tight oil, deepwater and oil sands resources • Less than one-quarter of global oil resources have been produced • Remaining oil resources can provide about 150 years of supply at current demand

So not to worry. Peak oil will not be reached in your lifetime, or in the lifetime of your children, grandchildren or greatgrandchildren. Well, that is if these estimates are correct.

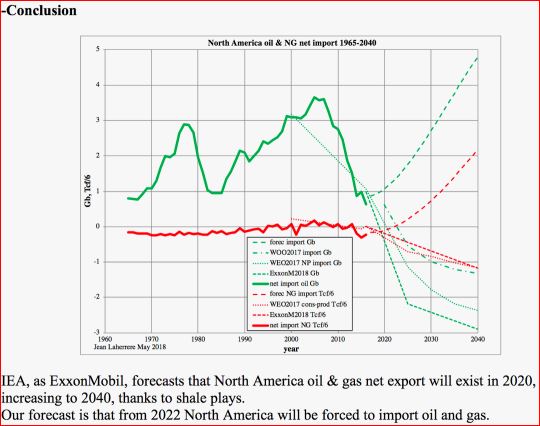

Jean Laherrere has a different outlook. He just posted me the below comments and chart. I could not get the chart to post in the comments section so I put it up here.

dear Ron

In your last good post on U.S. & World Oil Production and ExxonMobil OutlookYou mention the optimistic forecast by ExxonMobil on North America exportI sent you my last papers, which are on the site of ASPO France:

My conclusion is simple: for North America in 2040 the forecasts of EIA or ExxonMobil should change the sign of exports for oil and natural gas: instead of export it would be import.

US C+C production was up 231,000 barrels per day in June to 10,674,000 bpd, an all-time high.

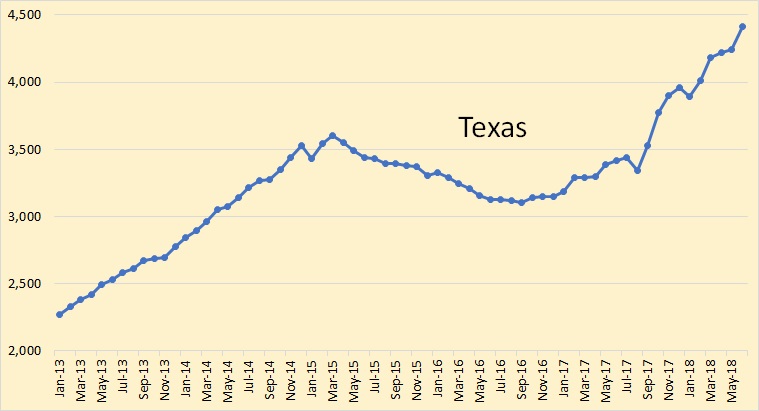

Texas was up 165,000 barrels per day in June to 4,410,000 bpd.

New Mexico was up 5,000 barrels per day in June to 657,000 bpd. The Permian extends into New Mexico.

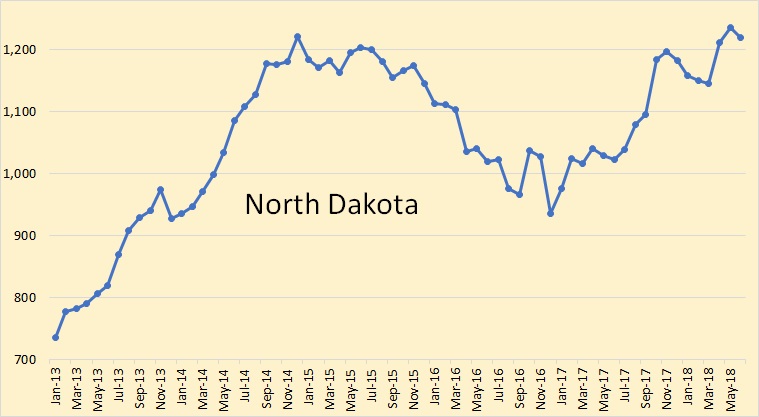

North Dakota was down 16,000 barrels per day in June to 1,220,000 bpd.

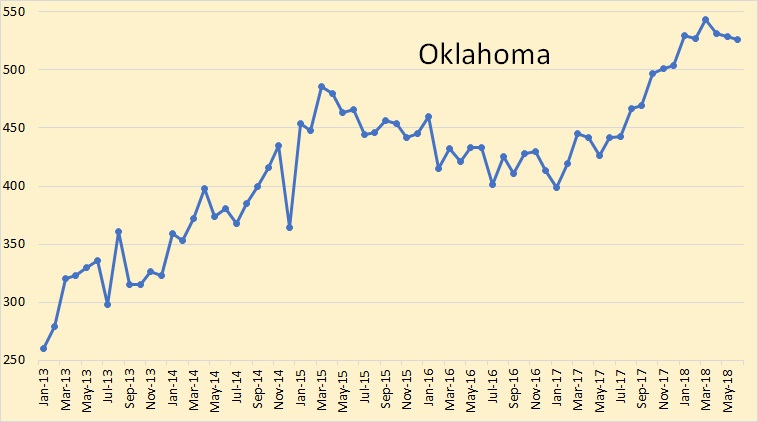

Oklahoma was down 3,000 barrels per day in June to 526,000 bpd.

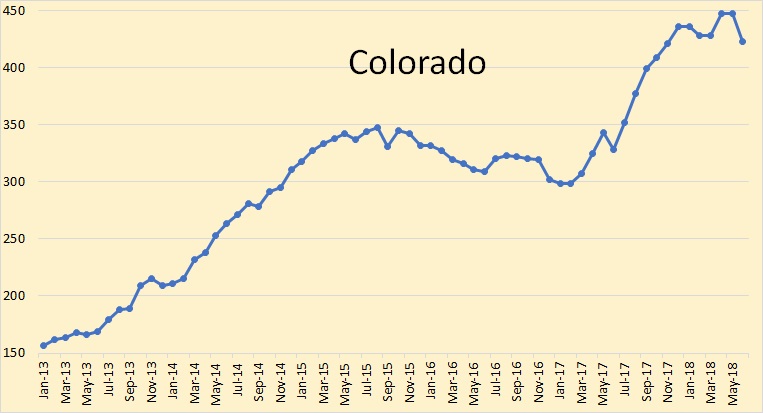

Colorado was down 24,000 barrels per day in June to 423,000 bpd.

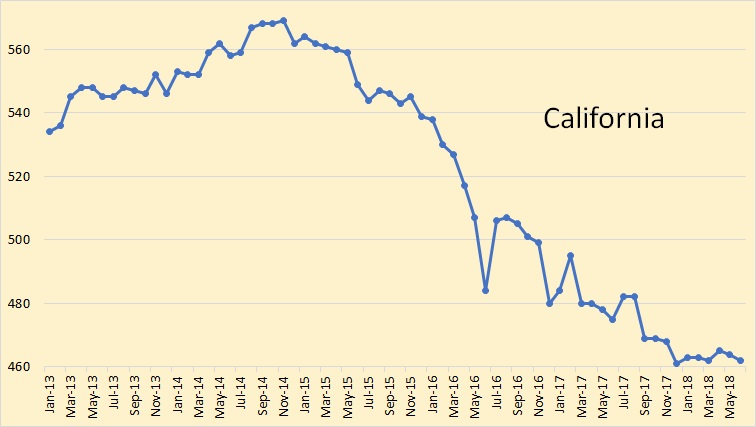

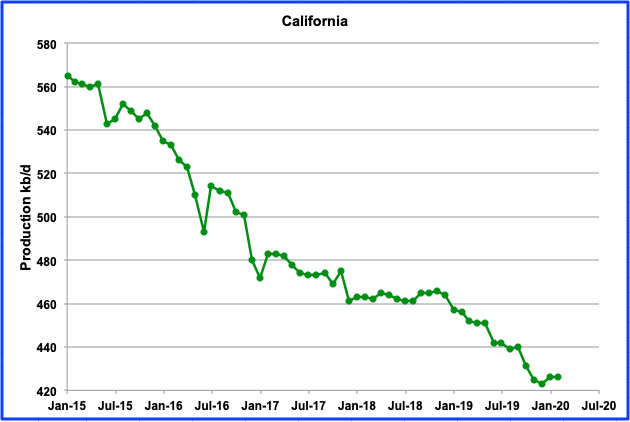

California was down 2,000 barrels per day in June to 462,000 bpd. California peaked in February of 1987 at 1,109,000 bpd.

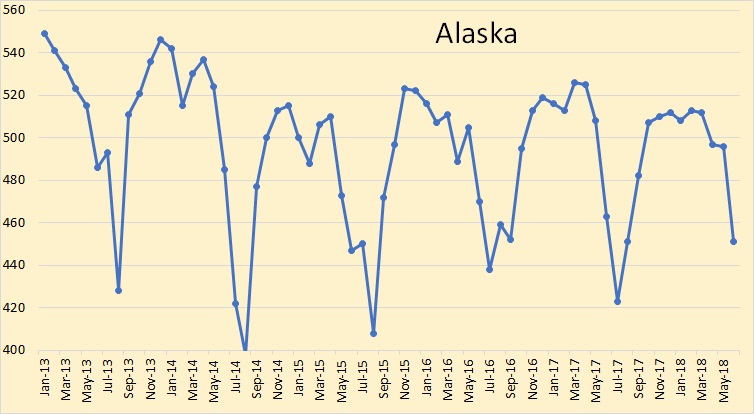

Alaska was down 45,000 barrels per day in June to 451,000 bpd. June, July, August, and part of September are the prime maintenance months for Alaska. The maintenance includes pigging the pipeline and overhauling the pumps along the pipeline.

The Gulf of Mexico was up 154,000 barrels per day in June to 1,658,000 bpd. Just a couple of years ago the EIA was predicting the GOM to be at almost 2 million barrels per day by now. I really don’t think that is going to happen anytime soon.

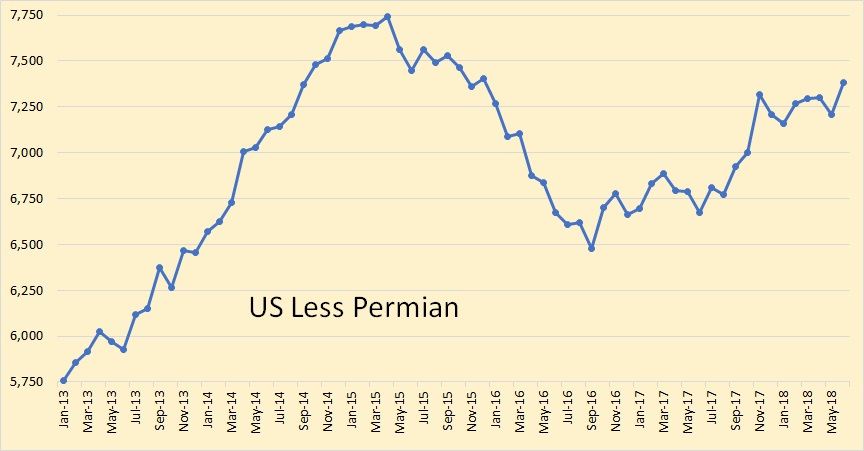

Using the EIA’s Drilling Productivity report for Permian production, through June, the US less the Permian, is still 357,000 barrels per day below the peak reached in April 2015. It is obvious that the Permian is the driving force behind the major increase in US production.

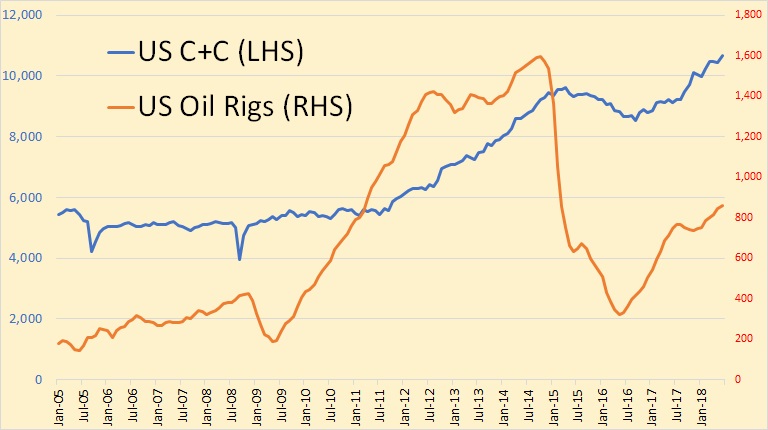

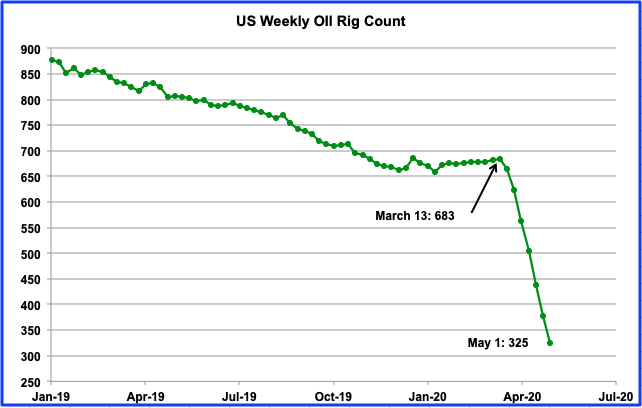

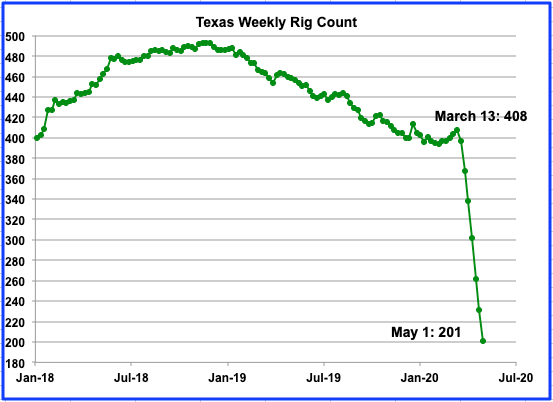

The above data is through June 2018. This is oil rigs only, no gas rigs.

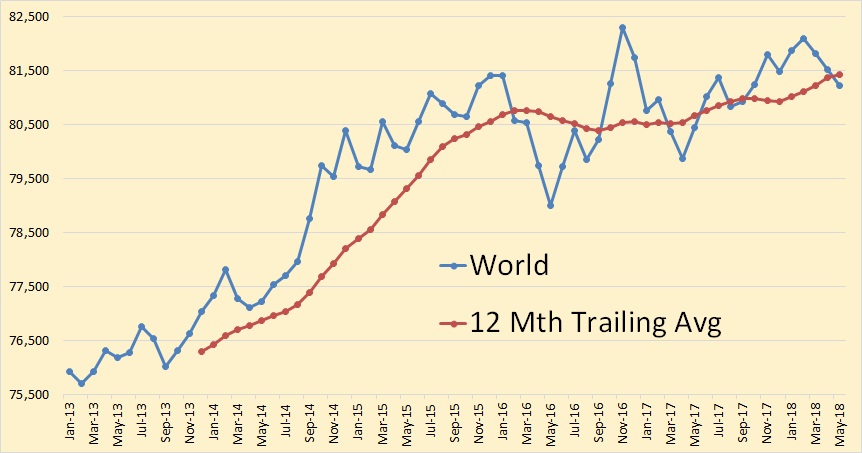

The numbers here are only through May 2018. We are obviously on that proverbial bumpy plateau. A prediction! I see world C+C production peaking around July or August, remaining level to slightly down for about two years, then begin a steady decline.

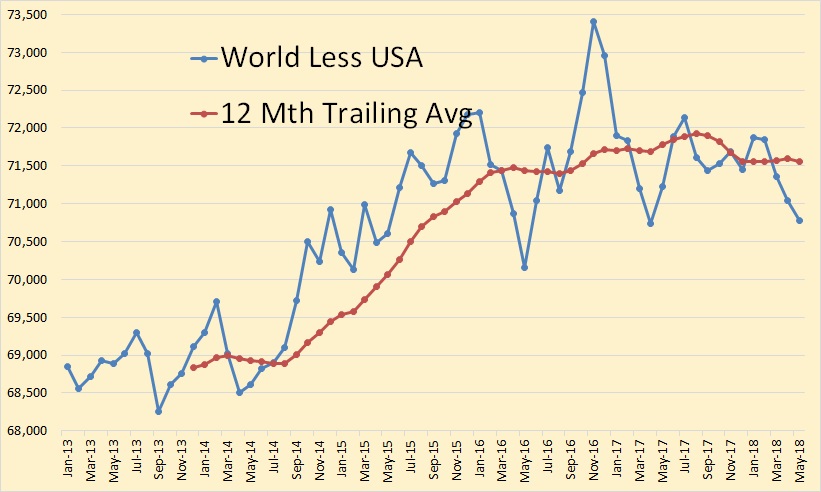

It all depends on the USA. The US, and to a lesser extent Canada, are the only nations that are still really growing by any significant amount. The US has increased production by 1.6 million barrels per day in the last 12 months, June 17 to June 18. Total world has increased less than half that amount.

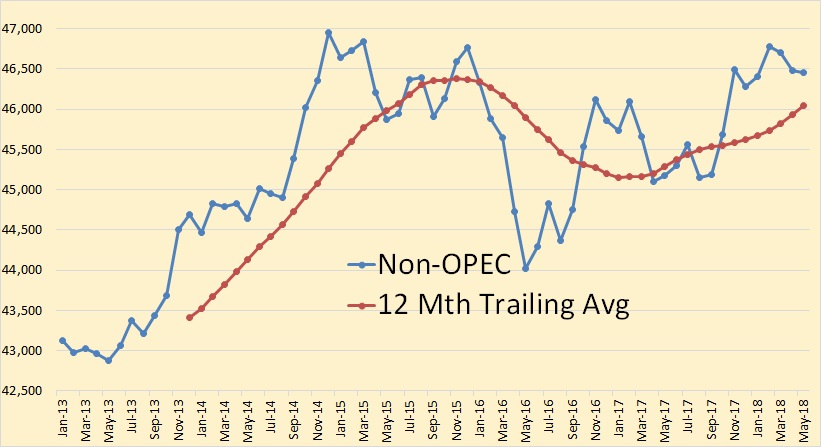

Non-OPEC is half a million barrels below its previous peak of December 2014. It may breach that peak later this year, but not by much.

Non-OPEC less USA is 1.5 million barrels below its previous peak of December 2015.

Canada EIA through May with Canada’s National Energy Board’s projection through December 2018.

China has slowed its decline somewhat.

The United Kingdom has, for now anyway, completely halted its decline.

Norway… well that’s Norway.

Mexico, for the time being, has slowed its decline.

This is the EIA’s estimate of all Persian Gulf production. That includes Saudi Arabia, the UAE, Kuwait, Iran, Iraq, Qatar, Bahrain, and Oman. This is through May. There will be a slight uptick in June, July, and August but will not likely breach the previous high in November and December of 2016.

This is Russia through August 2018 from the Russian Minister of Energy. They are now back to the level they reached in the last quarter of 2016.

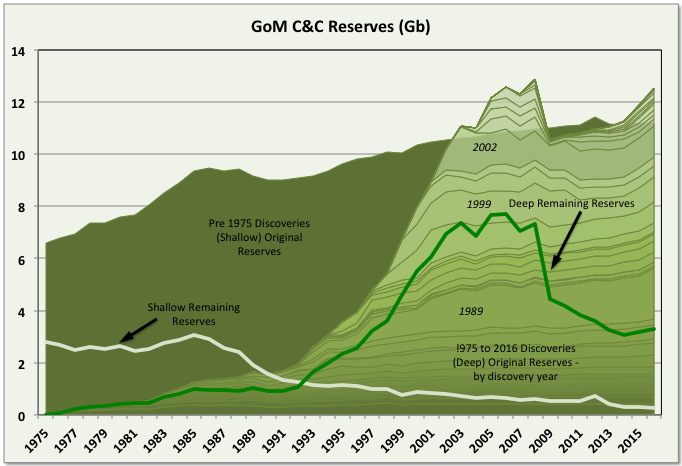

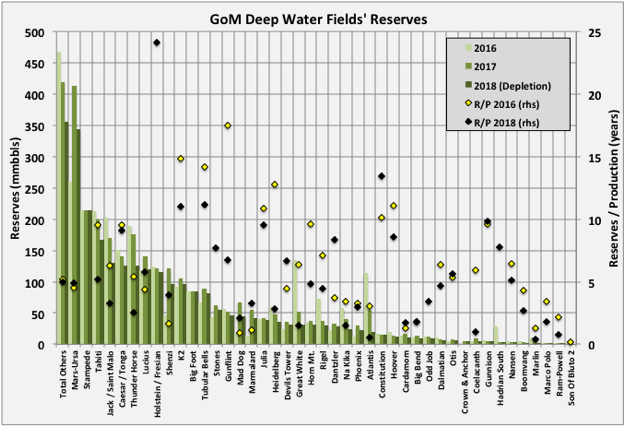

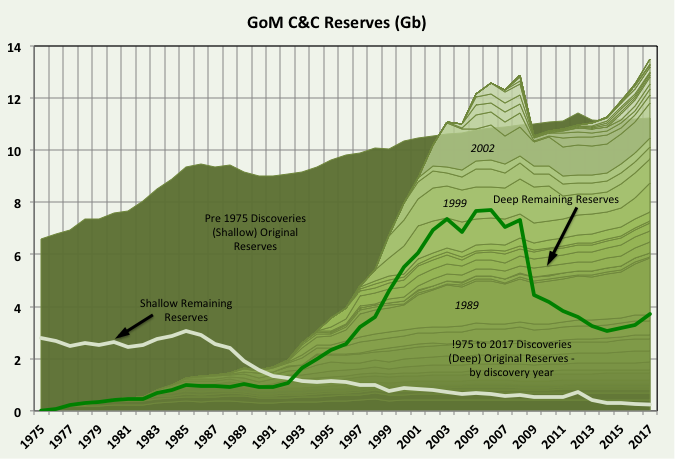

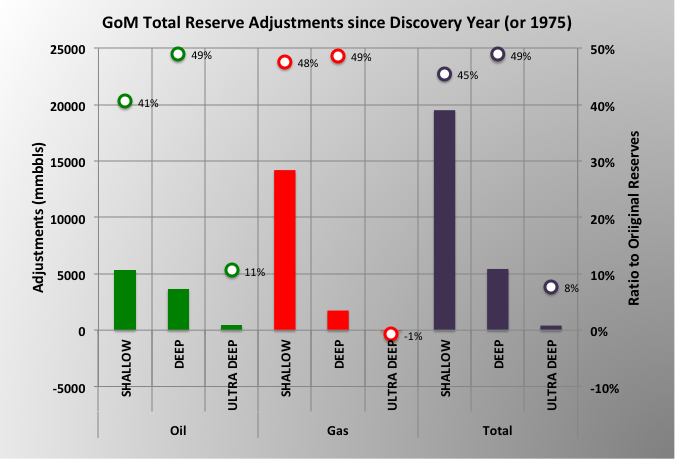

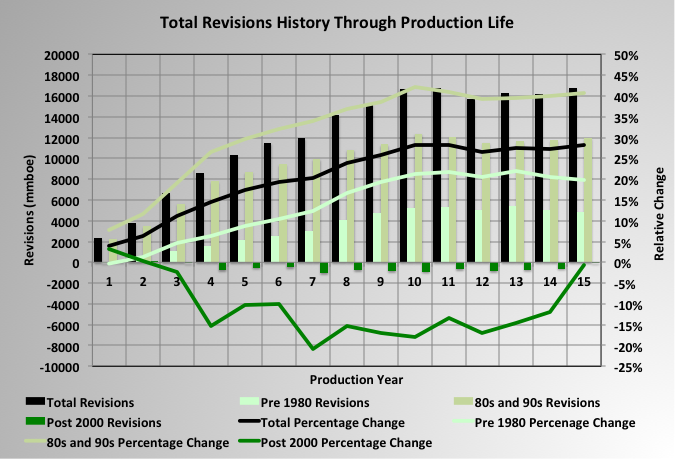

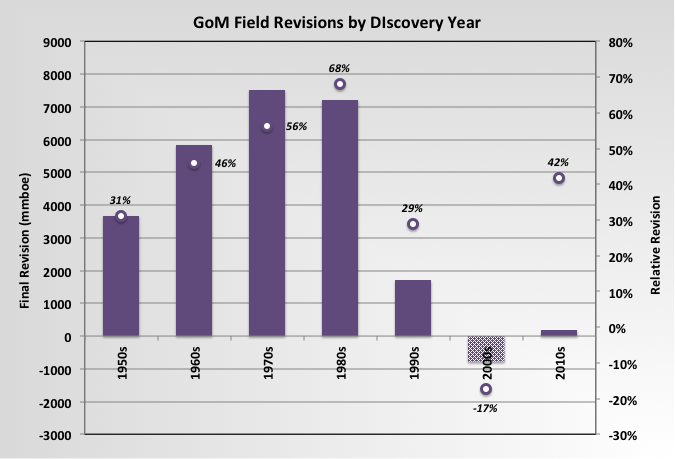

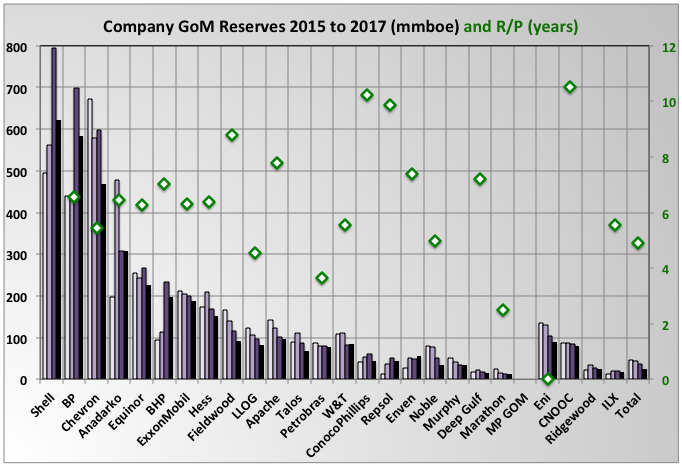

BOEM remaining C&C reserve estimates for GoM increased by 649 mmbbls for 2016 (i.e. to 31st December 2016). This was 112% reserve replacement and followed a similar growth of 618 mmbbls (111% reserve replacement) for 2015. The BOEM reserve calculation method appears to give highly conservative estimates. The increasing reserves followed several years, from 2006, of less than 100% reserve replacement, and actually negative numbers in 2006 and 2008. Current total original reserves (i.e. ultimate recovery) are a new high beating 2006 values, though deep water numbers are still below that year with the main growth appearing to be coming from: 1) older fields that were downgraded because of changes in SPE rules in 2007 (i.e. that reserves could only be booked if there were clear plans for their development within five years); and 2) newer discoveries, mostly smaller fields that are developed through tie-backs to existing hubs. These newer fields often do not get shown as new discoveries because BOEM records production and reserves against leases and each lease is recorded against a single field, even if there are deposits of different depth, age, geology and significant spacial separation within in it.

Current oil reserves are 3.569 Gb, which is 15% of the estimated original reserve (aka ultimate recovery). BOEM give the reserves as 2P (i.e. proven and probable) but they look very conservative and are actually lower than the EIA numbers, shown below, given for proven only and based on the operators own numbers, although the two are converging. The historical reserve histories look closer to how 1P (proven) numbers often appear, for example with some fields maintaining near constant R/P numbers, some showing large early drops that then come back over time, and some numbers being suspiciously low on fields obviously not near run out production rates (e.g. Mad Dog and Son of Bluto 2). I think the reserve calculations methods are fairly basic, given the amount of work required they couldn’t be much else, and use volumetric methods (i.e. reservoir area, depth, porosity, recovery factor) and previous decline data (I don’t now if the operators give them additional data such as well pressures).

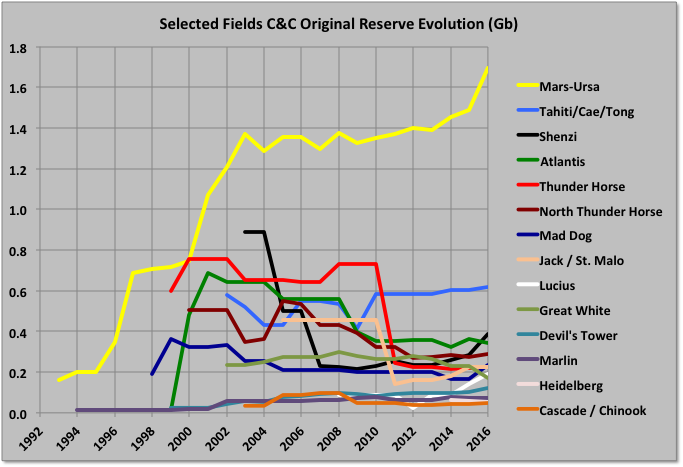

Reserve Evolution History

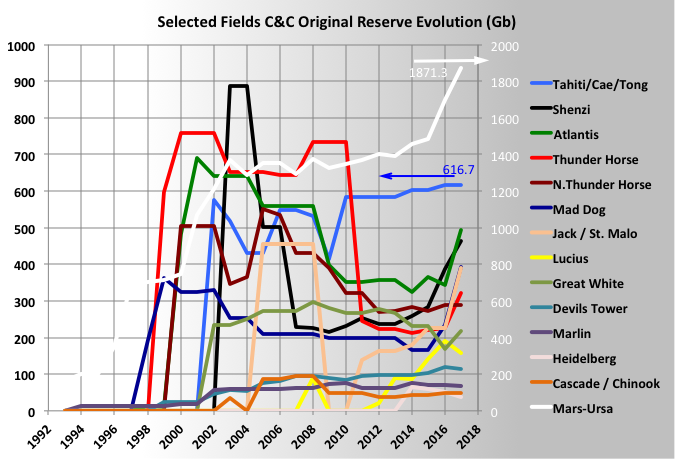

The Mars-Ursa fields have big original reserves, which have shown continuous growth. Other, large deep-water fields have mostly shown negative revisions from original reserve estimates, some quite large, though some of that is due to development timing (e.g. Mad Dog II reserves, when added, will likely recover all the earlier drop, and more). Shenzi has grown recently, and Atlantis will next year, both from new near field discoveries.

Individual Fields

The largest upward revisions in remaining reserves were for Shell’s Mars-Ursa field, which more than doubled the numbers (allowing for production). I think most of the gains came from new satellite fields at West Boreas and South Deimos, which are now on production, and possibly Kaikias, which has recently been started up. Other big gainers were Mad Dog, which had a very low number previously last year, and Shenzi, where BHP have made discoveries at Caicos and Shenzi North in the same lease blocks.

The largest downward revisions in ultimate recoveries were for Atlantis, Great White and Rigel. BP recently rescinded its lease at Rigel, which may be related, and the LLOG leases showed rapid decline rates before they went off line (presumably temporarily) because of the subsea manifold failure at Delta House. Great White has been gradually reduced in size by about 40% over the last ten years. Atlantis had a big write down in reserves after start-up, but BP announced a 200 mmbbls addition to resources in the area last year through new seismic technology, which is due to be developed in 2020 and presumably will be added in the next reserve numbers (in the mean time it looks likely the existing Atlantis wells will decline quite quickly).

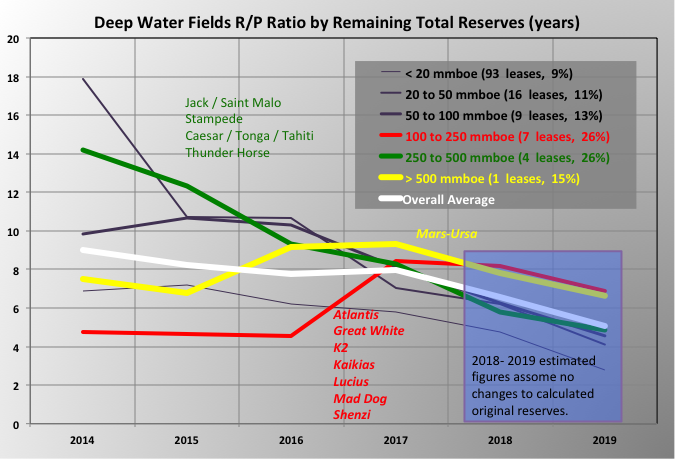

In the chart above the 2016 and 2017 reserves are the BOEM remaining oil reserves from the two latest estimates. The “2018 Depletion” data is the 2017 numbers less the 2017 production for that field, and the fields are ordered by that number. The R/P numbers are end of 2016 reserves divided by 2016 production, but for 2018 are the 2017 reserves less 2017 production divided by that production (to get the 2017 number add one to the R/P shown). Many R/Ps for the larger fields are in the range 4 to 6 years, which is equivalent to depletion rates, and therefore declines in exponential type well profiles, of around 16 to 25%, and that what has been typically seen recently. There are some very low numbers on fields with quite respectable production still, which probably indicates the reserves aren’t including some recent discoveries or revisions; for example Marlin has had recent tie-backs from Dorado and King fields, and Son of Bluto 2 (I don’t know what is happening there, it seems to be cycled now but in June cumulative production exceeded the recent BOEM original reserves estimate).

Caesar / Tonga and Tahiti are really a single field and BOEM report them as such, but it is spread over different leases and production is reported separately so I’ve prorated the numbers based on production.

The only two newly named fields for 2016 are small: Crown & Anchor at 5 mmbbls and Calliope at 2 mmbbls. Crown & Anchor production started through two wells in June and is likely to show fairly steep decline and a short life, maybe similar to Son of Bluto 2, also operated by LLOG. Similar small field tie backs are planned by LLOG for Claibourne, Red Zinger and Blue Wing Olive, though BOEM had no reserve numbers for these yet.

Hadrian South showed big relative downward revision, but still not enough as the field died without producing what was estimated (the difference in the natural gas estimates was much more marked than for condensate shown in the chart), I think some of the oil reserve shown is actually for Hadrian North and may now be shown against Lucius. The small Lena field showed an upward revision but actually has now been shutdown after no further production. Other, older fields showing significant growth were Who Dat, where subsea pumping is planned, and Crosby, I don’t know why but it is associated with Mars-Ursa and has production of only a few thousand barrels per day (the latest reserves and average 2018 production give it an R/P of almost 100 years).

Appomatox and associated fields were approved for development by Shell in 2016 so I’m unclear why they have not been included in the reserve numbers, presumably they will be added for 2017. The Mad Dog II project was approved last year, so that too should be added as well as the new Atlantis finds, therefore the replacement ratio should again exceed 100%, probably by more than the 2016 additions. After those there is Vito, approved this year, but then things will start to get leaner

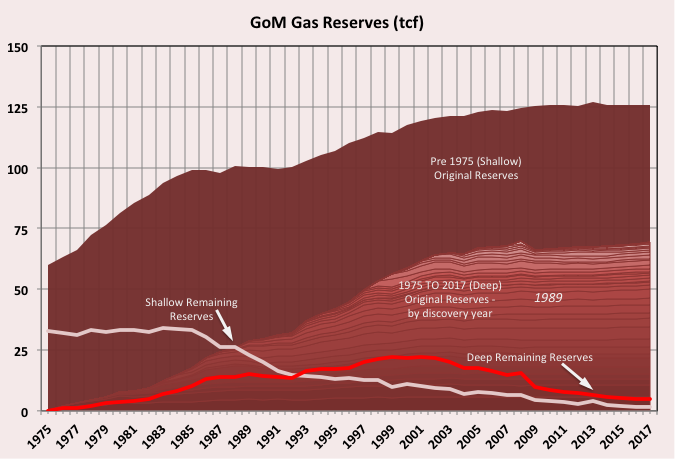

Natural Gas Reserves